The EU Foreign Subsidies Regulation

Subsidies made by non-EU countries are not subject to the European State aid regime. This has given rise to increasing concern about contributions made outside Europe that may distort competition within the EU. The FSR, which came into force on 12 January 2023, was adopted to close this gap, and tackle the potential distortive effects of foreign subsidies to ensure a level playing field for all companies operating in the EU.

The FSR adds three new tools to the European Commission’s regulatory arsenal.

- A compulsory notification system for M&A transactions that meet specified turnover and financial contribution thresholds.

- A compulsory notification system for companies bidding to obtain large public tenders where those companies have received foreign financial contributions.

- Powers that enable the Commission to conduct ex officio investigations into other foreign subsidies.

These tools are accompanied by sweeping powers to request information, sanction companies for non-compliance, and impose redressive measures to resolve any distortions of competition.

The FSR is cast broadly and captures a wide range of contributions, including capital injections, loans, guarantees, tax exemptions, contracts with public authorities, and private sector investments made by sovereign wealth funds and/or State-owned enterprises. Indeed, aid received by many businesses as part of Covid support packages and subsidies related to green initiatives, such as those proposed as part of the US Inflation Reduction Act, are likely to come within scope. The FSR also applies to all companies operating in the EU who are granted foreign financial contributions, including in connection with activities that are unrelated to the EU.

Accordingly, the FSR may require significant compliance efforts not only from groups that receive material amounts of ex-EU governmental support but also those that have material dealings with non-EU governments or State-owned enterprises.

Complying with the notification requirements will be burdensome. Companies that may be affected by the regime would be well-advised to already start working through its potential implications, and how best to identify financial contributions that are in scope (which may be particularly difficult for large corporate groups, private investment funds, and sovereign-wealth investors).

The Commission is expected to shortly launch a consultation on implementing rules, which will provide an early opportunity to steer the enforcement of this important piece of new legislation.

Merger notifications

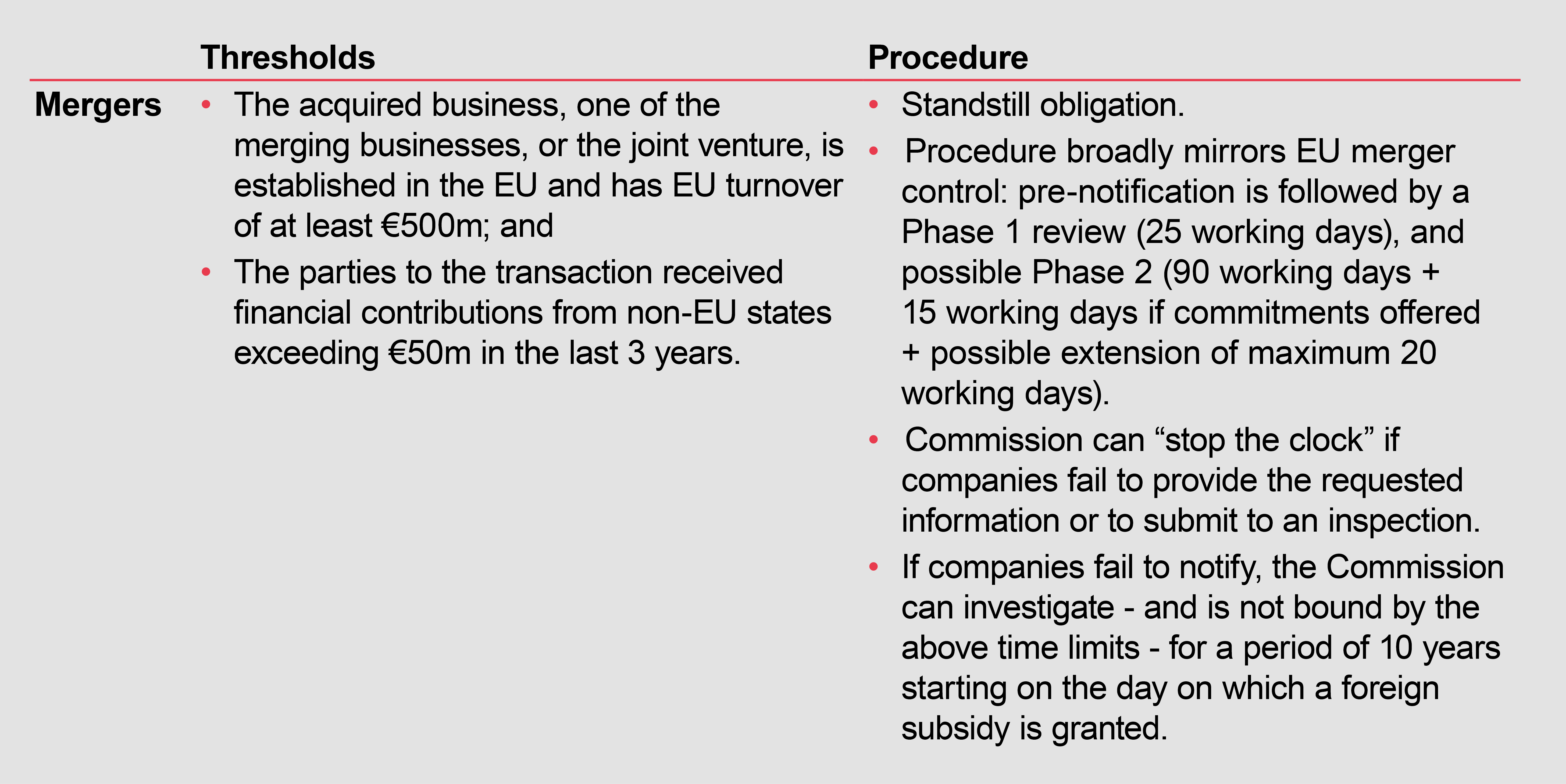

The FSR introduces a system of mandatory pre-closing notification and review for mergers, acquisitions and the creation of joint ventures that meet the following thresholds:

- the target, joint venture, or a merging party is established in the EU and has an EU turnover of at least €500m; and

- the companies involved in the operation received aggregate foreign financial contributions of more than €50m from non-EU countries in the three financial years prior to notification.

Several points bear mention as regards the calculation of foreign financial contributions.

- First, the concept is defined very broadly to include grants, capital injections, loans, guarantees, debt forgiveness, preferential tax treatment, and even the mere provision or purchase of goods or services (apparently even when tenders are awarded on normal market terms). In each case they need to take place with a non-EU government, public authority, or a “private entity whose actions can be attributed the third country, taking into account all relevant circumstances.”

- Second, all financial contributions received from outside the EU must be aggregated, so the value of contributions from a given country is not itself determinative.

- Third, the FSR takes account of all amounts received by the whole undertaking (a concept deriving from EU competition law); investment funds in particular will need to tread carefully in taking account of financial contributions received by controlled portfolio companies.

- Fourth, there is no need for a nexus between a financial contribution and the EU; the assessment of any potential impact in the EU is only relevant as part of the Commission’s substantive assessment.

Notifiable transactions cannot be implemented until they have been approved. The European Commission has 25 working days from receipt of a complete notification to carry out a preliminary assessment and decide whether to do so or to open an in-depth investigation in which case the standstill period is extended by 90 working days (which can be extended by a maximum of 20 working days and an extra 15 working days if the parties offer remedies). The Commission can, however, suspend those timelines if companies fail to provide requested information or submit to an inspection.

This timetable is broadly modelled on the EU Merger Regulation, such that both processes could in theory run simultaneously. However, synchronising the timelines will not always be possible, especially because the issues examined by the Commission under the FSR and EUMR will often be distinct. Moreover, the FSR does not yet provide for a simplified procedure as exists under the EUMR (though the Commission may still introduce such a system).

Public procurement notifications

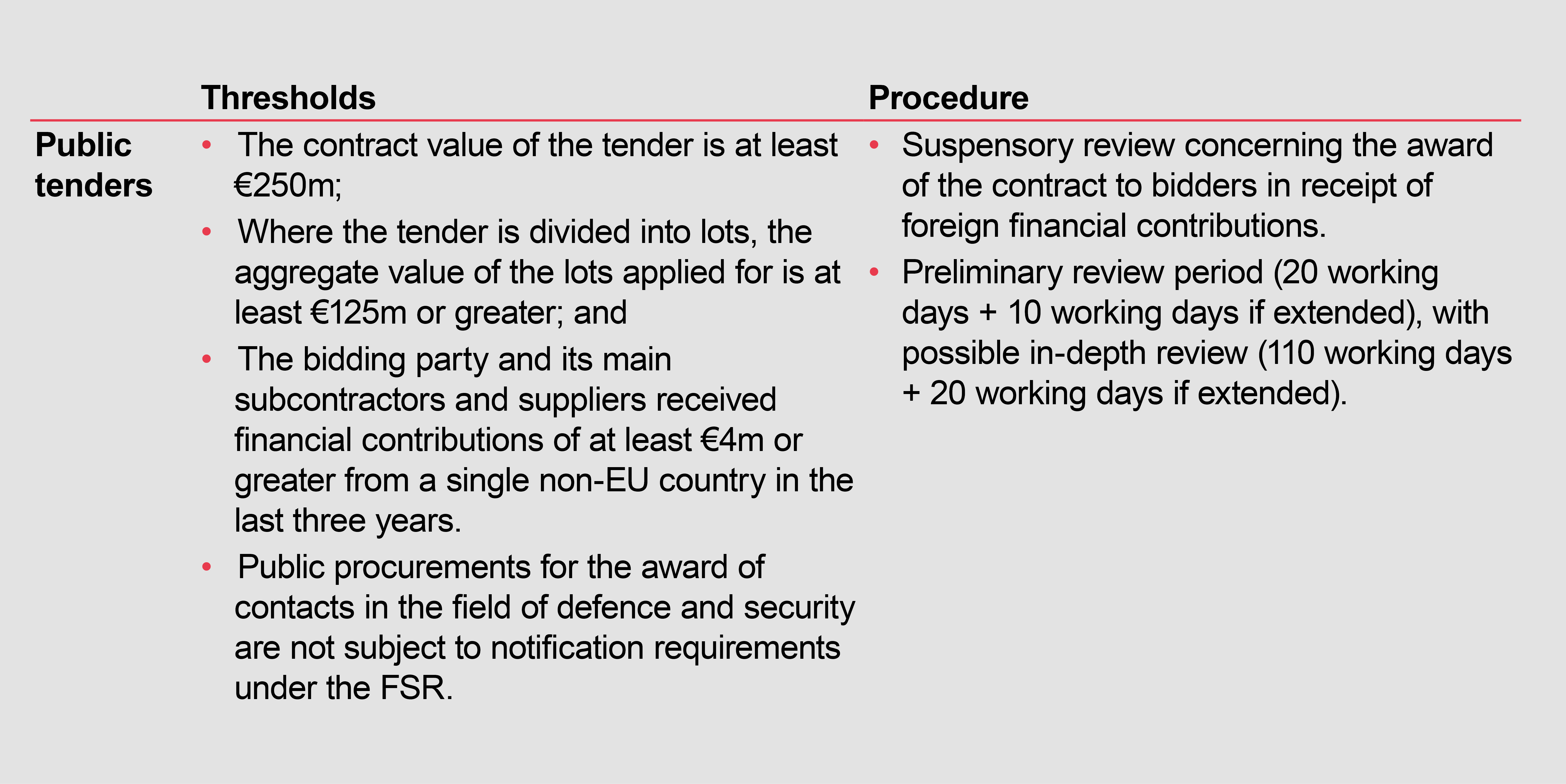

The FSR also requires bidders for public contracts to notify foreign financial contributions where the following thresholds are met:

- The estimated value of the public procurement or framework contract is at least €250m;

- Where the tender is divided into lots, the aggregate value of the lots applied for is at least €125m; and

- Aggregate foreign contributions of at least €4m per third country in the three financial years prior to notification are granted to the bidder involved in the tender (including subsidiaries, holding companies and, where applicable, main contractors and suppliers).

Companies that meet these criteria must notify the contracting authority of any foreign financial contribution received in the preceding three years or confirm that they have not received any such foreign financial contributions. In turn, the contracting authority will transfer the notification to the Commission.

This obligation is likely to prove particularly cumbersome for companies with significant dealings with governmental bodies. Indeed, since the notification obligation is triggered for each notifiable tender, a bidder could in theory find itself subject to parallel investigations if it simultaneously participates in several notifiable tenders. There may also be instances where an in-depth FSR investigation could create a tension with a desire for a public procurement process to run swiftly, including if it complicated efforts by the contracting authority to narrow the field of potential bidders through a staged evaluation process. In such cases, care will be needed to ensure that the bidder’s rights to equal treatment under the public procurement regime are not prejudiced by the FSR process.

Ex officio investigation tools

Finally, the FSR empowers the Commission to launch reviews of its own initiative to assess potentially distortive subsidies. These ex officio investigations will, amongst other things, allow the Commission to investigate foreign subsidies in transactions and public procurement procedures that fall below the notification thresholds described above. That said, the FSR does provide that foreign subsidies are not distortive if the total amount received does not exceed €200,000 per non-EU country in any three-year period, and are unlikely to raise concerns if the total amount received by the beneficiary does not exceed €4m.

If, after a preliminary review, the Commission has sufficient indications that a company has been granted foreign subsidies, it can open an in-depth investigation. Although the FSR provides that the Commission should aim to complete its in-depth investigation within 18 months, this is not binding. The Commission can investigate subsidies for a period of 10 years after they have been granted, including subsidies granted in the five years preceding the entry into force of the FSR.

Substantive assessment

Whereas the notification obligations are determined with reference to the value of financial contributions that have been received, the Commission can only take redressive action with respect to foreign subsidies. This latter concept mirrors the definition of State aid under the EU State Aid rules, and comprises four cumulative criteria.

In assessing the impact of any foreign subsidy, the Commission will consider whether it is likely to distort the internal market (e.g., by improving the competitive position of the recipient) and the extent to which such a distortion is counterbalanced by any positive effects on economic activity in the EU and/or EU policy objectives. In doing so, the Commission will take into account the amount of the subsidy, its nature, the “situation” of the undertaking (including its size and the markets at issue), the level of the undertaking’s economic activity in Europe, and the purpose and conditions attached to the subsidy and its use in the internal market. The FSR also provides guidance on when a subsidy is likely or unlikely to be distortive, as summarised below.

- aid to a failing firm which would otherwise exit the market (unless there is a viable restructuring plan);

- unlimited guarantees for debt and liabilities regarding amount and duration;

- a subsidy which directly facilitates an acquisition or merger;

- a subsidy which enables a company to submit an unduly advantageous public tender; or

- certain export financing measures that are not in line with officially supported export credits.

- does not exceed €4m;

- does not exceed €200,000 per non-EU country;

- over any consecutive period of three years; and

- if aimed at repairing damages caused by natural disasters or exceptional occurrences

The “distortive” categories of subsidy mirror those that are regarded as problematic under the EU’s own State aid regime, though it remains to be seen to what extent the FSR regime will be aligned with the established case law and practice in the area of State aid. However, as with the EU State aid regime, the Commission has a wide margin of discretion and the FSR regime will invariably involve a degree of uncertainty, at least in its early years of application.

Enforcement

Where financial contributions are investigated, the Commission has to decide whether to adopt a no-objection decision, a commitments decision or a prohibition decision. Specifically, where the negative effects of a subsidy outweigh the positive effects, the Commission can impose redressive measures or accept commitments from the parties concerned, such as:

- offering access to an infrastructure or facility on fair, reasonable, and non-discriminatory (FRAND) terms;

- reducing capacity or market presence;

- refraining from certain investments;

- licensing assets acquired or developed with the help of foreign subsidies on FRAND terms;

- publication of R&D results;

- divestment of assets;

- adapting governance structure;

- dissolving a concentration; and

- repaying the foreign subsidy.

As the FSR’s sole enforcer, the Commission will also have significant investigative powers and can request information from companies and carry out on-sight inspections, including outside the EU so long as the third country government has no objections.

The Commission’s powers to carry out preliminary reviews and in-depth investigations are subject to a ten-year limitation period, starting on the day on which a foreign subsidy is granted. However, opening a preliminary review, sending an information request, or carrying out an inspection interrupts the limitation period, after which a new limitation period starts to run afresh.

The Commission can impose fines of up to 10% of group turnover for violating the notification and/or standstill obligation, for implementing a prohibited transaction, or for failing to notify foreign subsidies in public procurement procedures. The Commission can also impose fines of up to 1% of the aggregate annual turnover for, intentionally or negligently, providing incorrect or misleading information. Periodic penalty payments of up to 5% of average daily aggregate turnover can also be imposed to force compliance with the FSR.

Conclusion

The FSR introduces an additional layer of regulatory complexity for many companies active in the EU. In particular, the notification obligations will be burdensome, particularly for those with a number of portfolio companies within their group and/or those with a large geographic footprint, who will need to carefully consider what contributions may have been received in each territory.

Companies that may be subject to the regime could already start to prepare for the full implementation of the FSR and possible future analyses and notifications, including through:

- involvement in the Commission’s imminent consultation process on the implementation of the regime;

- carefully consider the FSR regime when participating in public tenders and in the conduct of M&A activities (including the potential impact of the new rules on transaction timelines, due diligence, and the drafting of condition precedents in corporate transaction agreements);

- designing internal processes for the collation of information on foreign financial contributions across their group over the past three years. Particular care should be taken for jurisdictions where the line between governmental bodies and private entities is blurred; and

- evidence should also be collected to show whether transactions involving financial contributions are made on market terms and hence do not give rise to a subsidy. Where it is unclear if this is the case (e.g., whether a particular aspect of a foreign tax regime is considered to constitute a selective advantage), a broad range of evidence could be relevant, such as fairness opinions, independent expert reports, and proof of a competitive tender.