/Passle/5a1c2144b00e80131c20b495/MediaLibrary/Images/2025-10-03-11-18-50-250-68dfb11a8a133db117a65ab9.jpg)

Key issues to consider when private credit is given the keys to a borrower

10 minute read

As private credit has increased its dominance over recent years, particularly in the financing of mid-market deals, so too has risen the number of stressed and distressed situations in which private credit fund lenders find themselves as key creditor. Whilst this increase comes simply as a corollary to the growing footprint of private credit it poses new challenges to those private credit fund managers who may not have previously had experience in this area.

For the most part in instances of borrower stress/distress private credit fund lenders often take a relationship-based approach to borrowers and their sponsors and will be open to granting waivers where breathing space is needed. However, where they cannot, for example where there is a liquidity need and the sponsor is not willing to provide that financial support to the borrower, the private credit fund lender may feel it has no choice but to take control, whether that be consensually or otherwise.

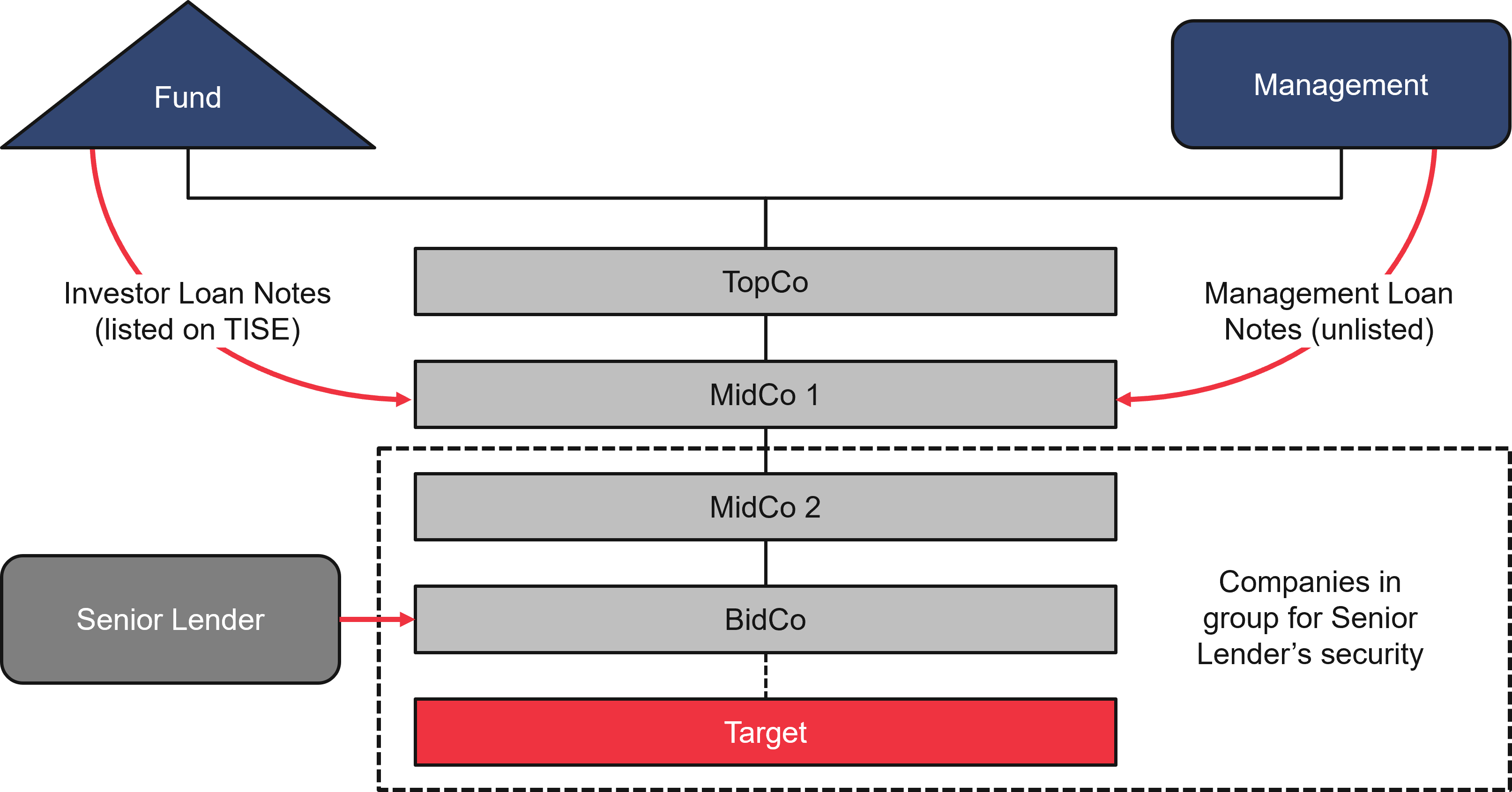

In this note we examine the primary issues for private credit fund lenders in a typical unitranche/super senior structure (i.e. those private credit funds acting as sole lender of a term facility alongside a super senior working capital facility) (see Figure 1) when they are considering taking the keys to a borrower. We discuss how a private credit fund lender might minimise disruption and create a stable platform from which to take control of equity, including the options available to them to push through a transaction if the borrower/sponsor is not cooperative, as well as associated tax, due diligence and deal term considerations.

Figure 1: A typical buyout structure

How can a private credit fund lender minimise disruption and create a stable platform from which to take control of a borrower?

A key to the success of any change of control of a borrower is first ensuring sufficient stability and that, notwithstanding the impending removal of the sponsor, disruption is minimised and day-to-day operations are maintained. Private credit fund lenders ought to consider:

Directors’ duties: are the directors of the borrower properly advised?

Whilst private credit fund lenders will be keen to ensure that they are not considered shadow directors (i.e. that they merely provide indications of the actions that would be necessary to maintain their support, subject to the independent judgment of the board), it is also important in any situation of stress/distress that the directors have access to comprehensive advice. For example a private credit fund lender might invite directors to hire a specialised Chief Restructuring Officer to help them navigate the various stakeholder management aspects of the process of which they might not otherwise have experience.

Of particular note, directors ought also to be mindful of wrongful trading, which occurs when a director continues to trade a company after they knew, or ought to have known, that there was no reasonable prospect of avoiding insolvent liquidation or administration. If found to have traded in this way directors would be personally liable for the worsening of the position of the company's creditors unless they have taken every step to minimise losses to those creditors.

Expecting the unexpected: are appropriate contingency plans in place?

Private credit fund lenders will be keen to ensure that the board has appropriate contingency plans in place, from ensuring an appropriate PR strategy has been developed in the event of information leaks, particularly where the business in question is one with name recognition, to implementing a strategy to keep employees and other creditors suitably incentivised and managed.

Early stage tax planning: collaborative engagement

Whilst there ought not be significant tax issues in a UK group in stress/distress (of the type described in Figure 1) in respect of its day-to-day corporation tax liabilities, where a private credit fund lender looks to take control of equity in that group that might have serious tax ramifications. Typically borrower side tax advisers, with ready access to company information, would hold the pen on tax planning. However early stage collaborative engagement and information sharing between the private credit fund lender and borrower teams is key to identifying and navigating potential tax impact.

Deemed release rule

A key issue to determine, and one which turns in part on the treatment by the private credit fund lender of the borrower’s debt, is whether “deemed release” rules are likely to apply to the overall transaction.

A private credit fund lender will typically want to keep the borrower’s debt as unimpaired as possible in order to retain its senior secured claim over the borrower group. However, it is likely that the private credit fund lender will at an appropriate time impair the borrower’s debt on the private credit fund lender’s own balance sheet in order to reflect the stress/distress in the borrower.

Deemed release of impaired debt occurs where a lender holds impaired debt and becomes connected with – has control over or is subject to the same common control as - a debtor company. In the event of such connection there is deemed to be a taxable credit in the debtor company (subject to the availability of certain exemptions/use of losses).

The deemed release rule that applies where lenders and borrowers become connected turns on how the lender entity(ies) accounted for the debt at the end of the accounting period immediately before the one in which the connection arose. Broadly, the rules apply if the lender had impaired the debt in the immediately preceding accounting period to the connection. Whether these rules already apply, or might in the future do so, can have a material impact on the timing imperatives of any restructuring transaction.

Due diligence

Taking control of shares in the borrower on a restructuring in the event of borrower stress/distress is clearly different from a typical M&A process as the private credit fund lender is already effectively “invested” in the company. However private credit fund lenders taking the keys will often want to ask some high-level tax diligence questions that aim to establish whether any serious instances of non-compliance have occurred or matters which pose a potential reputational issue, such as non-compliance or tax avoidance on the tax front exist.

How can a private credit fund lender push through a restructuring takeover transaction if the borrower/sponsor is not cooperative?

Where a sponsor is uncooperative with a private credit fund lender in a restructuring scenario and is unwilling to hand over the equity on a consensual basis, the private credit fund lender can nonetheless effect a restructuring takeover by implementing a number of the other tools and processes at its disposal. However, preparation is key: the performance of a sufficient level of due diligence can help ensure that the private credit fund lender avoids any nasty surprises occurring as a result of the takeover transaction.

Enforcement: fail to prepare, prepare to fail

When considering any restructuring process it is important that private credit fund lenders perform an early analysis of the security package that they hold vis-à-vis the borrower in order to be aware of what action they might take, and in respect of which assets. As part of this security review the private credit fund lender will wish to ascertain whether there a single point of enforcement that allows the private credit fund lender to take control of the entire Borrower group in one go.

Where this option is either not available or is undesirable, enforcement will usually involve a more complex process of multiple enforcement proceedings over the business and assets of the borrower group: cherry picking which assets are to be subject to the proceedings and which are associated with liabilities that the private credit fund lender may wish to leave behind. Among other things the private credit fund lender will consider:

- Intercompany debts: are there any intercompany debt claims into the Borrower from companies “left behind” that are not released on enforcement? If yes, are there means to work around them if need be?

- Assets: what are the key assets of value in the borrower? Is enough information about them available? Are there any assets that are not attractive and ought to be left behind, for example land with an environmental or planning liability?

- Impact of enforcement: what effect would enforcement and/or a change of control have on the value of key assets?

- Method of enforcement: in which jurisdiction are the assets located and will this have an impact on the process and timing for enforcement? How is enforcement going to be effected and by whom? Does the appointed security agent have any specific requirements, such as the provision of an indemnity and/or independent legal advice?

Business continuation

It will also be important for a private credit fund lender to plan for the impact that taking control of the borrower might have upon the business of the borrower.

- Ensuring continued provision of essential services: private credit fund lenders will be keen to ensure that the provision of services essential to the business of the borrower are not impacted by the takeover and if there is any potential impact, how that might be planned for/mitigated against. In particular, who are the providers of essential services to a business? Can they exit if there is a change of control? Might they increase fees?

- Overview of borrower liabilities: it will be important to have a full understanding of the current and future liabilities of the borrower and consider the risk of “contaminating” a lender, which can for example occur in relation to pension liabilities, liabilities under the Building Safety Act 2022 and/or environmental liabilities.

- Future governance arrangements: how will the private credit fund lender maintain its influence on the board? Will it look to appoint nominee directors or restrict the board in respect of certain reserved matters (over the above controls under their finance documents)?

- Tax: in addition to any early tax planning and consideration of the tax impact on the borrower, assessment of the tax impact of the restructuring takeover on the private credit fund lender, and whether equity in the borrower ought to sit with the private credit fund lender or another entity, is key.

Implementing the restructure: once the plan is set, what happens next?

Once the restructuring takeover is effected, the private credit fund lender holds the equity of the borrower and has taken control, what then?

Reworking the debt documents

It is a decision for the private credit fund lender as to whether the debt documents documenting the debt between the private credit fund lender and the borrower ought to be reworked following a restructuring takeover.

It would be unusual for the private credit fund lender to loosen the debt documents significantly. However, given that following the restructuring takeover the private credit fund lender will control the borrower, the private credit fund lender will need to waive any breach of, and update, change of control provisions and reschedule amortisation (if applicable). The private credit fund lender may also look to loosen financial covenants which, save for the liquidity covenant, are likely to have decreased in utility given that post the restructuring transaction the private credit fund lender owns the borrower, has direct access to borrower information and is likely privy to significant decisions of the board.

If not already available, it is not uncommon for the private credit fund lender to update the debt documents to include a short-form accordion facility mechanic to enable the provision of a further funding as the new management of the business find their feet.

Balance sheet restructuring

Typically, and in addition to a restructuring of equity, a group in distress will require a balance sheet/operational restructuring (often in conjunction with a reset of a management incentive plan). Whilst this restructuring might be effected by a comprehensive renegotiation of its key liabilities and contracts on a consensual basis, this approach would take a not insignificant amount of time and would come at considerable cost with no guarantee of success. Lenders could instead use a restructuring plan under Part 26A of the Companies Act 2006 to restructure a borrower’s balance sheet in a far more efficient manner alongside taking equity.

Restructuring plans can be used to implement a range of arrangements including to exit unprofitable leases, reduce rents, terminate unwanted contracts and write-off sums owed to HMRC. Notably, and unlike schemes of arrangement, restructuring plans can overcome significant opposition to a restructuring from creditors as the court has the power to sanction a restructuring plan even where an entire class of creditors or shareholders has voted against it.

The use of a restructuring plan requires a larger amount of work up front, but its use can effect a balance sheet restructuring without ongoing discussions, and once sanctioned can allow the borrower and its private credit fund lender owner to get on with the turnaround of the business. It is this comprehensive approach that we think will be attractive to private credit fund lenders looking to acquire control of borrower groups in the future.

| For more on restructuring plans see Restructuring plans - dos and don'ts and Restructuring plans - do's and don'ts (part 2): lessons from 2024. |

Authors

Related topics

Like what you are reading?

Stay up to date with our latest insights, events and updates – direct to your inbox.

How can we help you?

Browse our people by name, team or area of focus to find the expert that you need.