/Passle/5a1c2144b00e80131c20b495/MediaLibrary/Images/2025-10-03-14-34-49-044-68dfdf096272d0dedd551605.jpg)

Rethinking European defence: Market dynamics and sector opportunities

8 minute read

Shifting global geopolitics are rapidly increasing European defence spending, creating space for private capital funds (PCFs) and institutional investors. This first report analyses these market dynamics, highlighting why investors increasingly view defence as a strategic opportunity rather than simply a risk, with a particular focus on key industry verticals downstream of controversial weapons.

Overview

Recent shifts in global geopolitics have prompted a significant reassessment of defence spending priorities across Europe, where countries face increasing pressure to take greater responsibility for their security. Governments across the continent now require new technology platforms, upgraded infrastructure, and expanded supply chains to rebuild defence capabilities to meet growing threats.

Institutional investors and private capital funds can play an important role in this effort – major asset managers like Aviva1 and Legal & General2, for example, have signalled increasing engagement in the sector, supported by reforms in European regulations enabling private capital participation.3 The UK's recent Comprehensive Spending Review demonstrated this commitment with substantial increases in defence capital spending4, whilst exploring broader pension fund investment into the sector.5 Germany has issued guidelines clarifying that sustainable finance regulations should not restrict defence industry financing6, and progress on EU-UK defence cooperation agreements could enable enhanced access to European Defence Fund opportunities for UK manufacturers.7

The defence sector encompasses a diverse ecosystem of technologies and services that extend beyond offensive capabilities to include protective systems, secure communications, and critical infrastructure that supports both military and civilian applications. While controversial weapons systems often dominate public discourse, this report focuses on the broader defence ecosystem and opportunities further down the value chain that can align with responsible investment frameworks.

In the next section of the report, we dive into the spending data that demonstrates both the urgency of current requirements and the sustained nature of future commitments.

Understanding the market

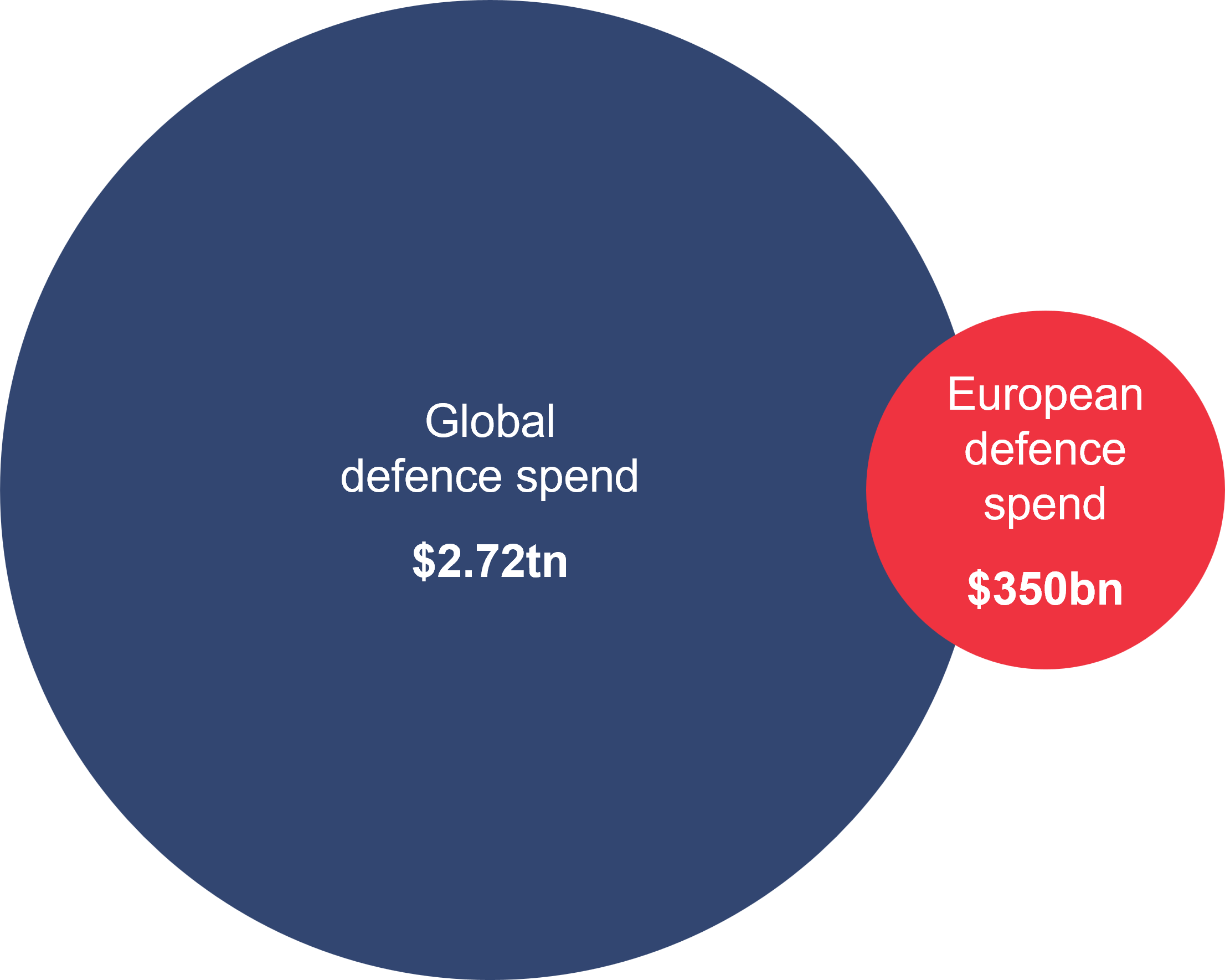

Defence spending, 2024

Global defence spending reached $2.7tn in 2024, representing 9.4% growth – the steepest increase since the Cold War ended.8 Major asset managers like Aviva have built upon this momentum, investing £900m in UK defence companies2 whilst Legal & General has announced substantial new commitments.9

The acceleration in European defence spending appears more pronounced than global trends, with EU member states allocating €326bn to defence in 2024 – a 30% increase from 2021 levels. Defence investments reached €102bn in 2024, with equipment procurement alone amounting to €90bn, representing a year-on-year increase exceeding 50%.10 The scale of this European commitment suggests structural rather than cyclical change, driven by fundamental reassessment of security requirements.

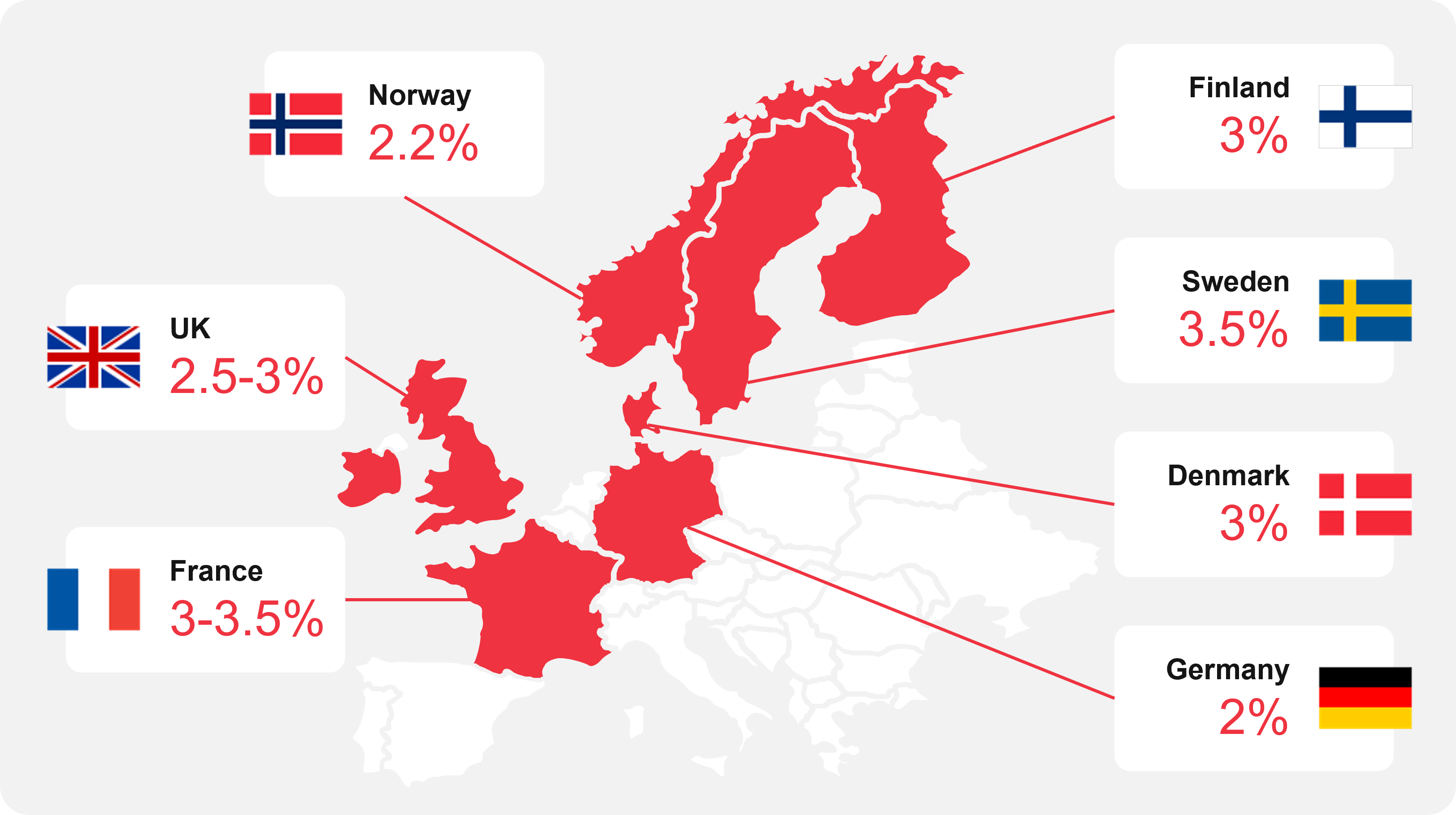

NATO defence spending transformation

Individual country commitments reveal the breadth and depth of European defence spending transformation. Major NATO members have announced fundamental restructuring of fiscal priorities that are likely to generate sustained demand for private capital:

Current defence spending commitments as a percentage of GDP

Germany

- Announced plan to exempt defence spending from constitutional "debt brake".11

- Issued political guidelines ensuring ESG standards do not restrict defence investment.12

- German financial associations (BVI) removed >10% revenue threshold for defence exclusions.13

United Kingdom

- Committed to increase defence spending to 2.5% of GDP by 2027, with ambition for 3% in next parliament. Represents potential £19bn increase from 2024 levels.14

- FCA clarified that ESG rules do not prevent investors with ESG mandates from investing in defence assets.15

France

- President Macron stated ambitions to raise defence spending to 3-3.5% of GDP (over €40bn increase).16

- AMF introduced accelerated approval process for investment funds targeting defence sector.17

Nordics

- Norway: Planning to nearly double defence spending by 2036, with pressure to allow $1.8tn sovereign wealth fund defence investment.18

- Sweden: Committed to 3.5% of GDP (from 2.4%)19, with Swedish defence fund becoming first Article 8 classified in Europe.20

- Finland: NATO member since 2023, committed to 3% of GDP by 2029.21

- Denmark: Plans over 3% of GDP over the next decade with dedicated fund for military capabilities.22

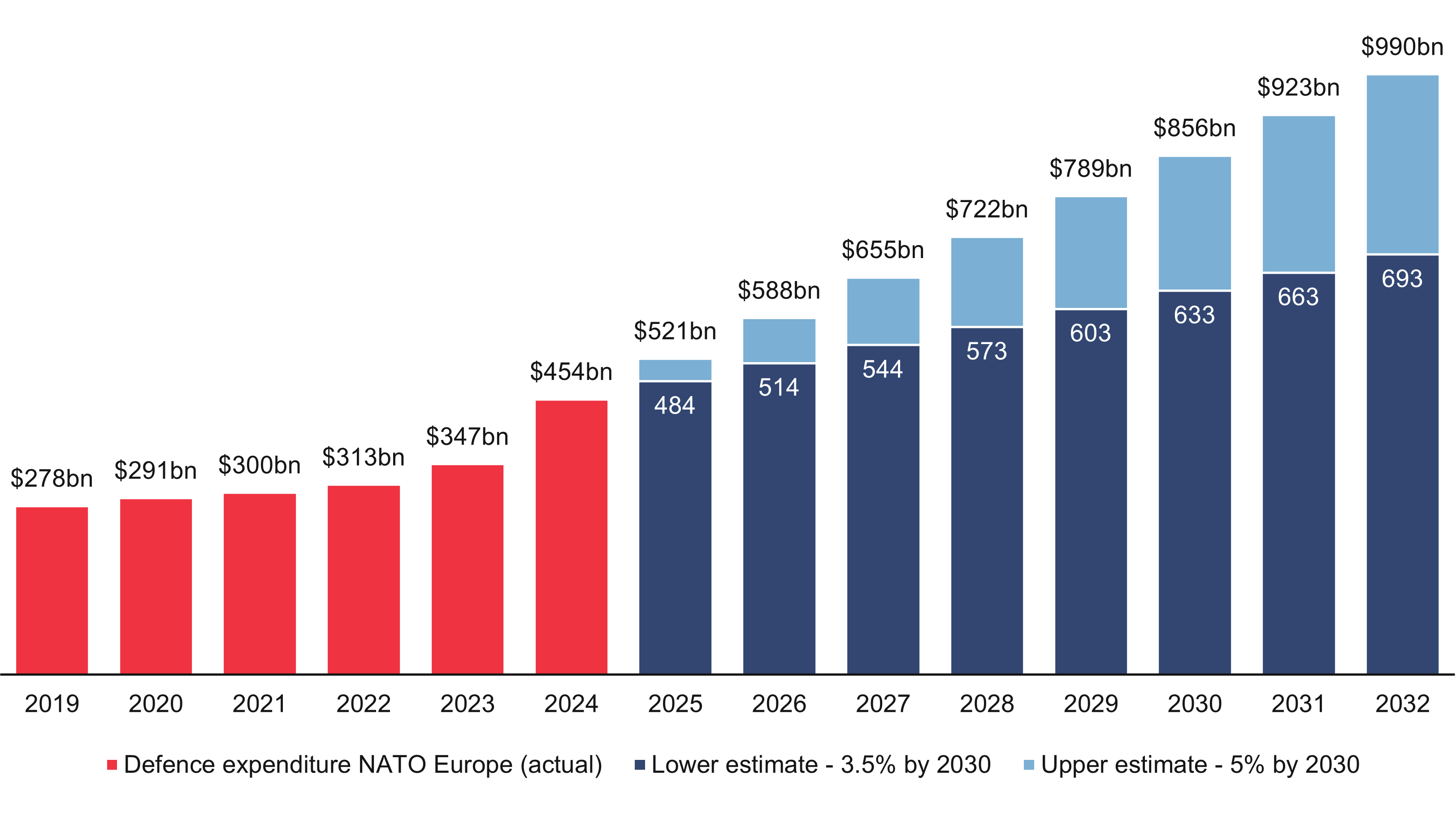

A new target for defence expenditure is expected to be agreed at the NATO summit hosted today, June 24, 2025. Secretary-General Mark Rutte indicated that this would include a primary target of 3.5% of GDP for direct military spending and an additional 1.5% for broader security-related investments, including infrastructure and cybersecurity.23

If a 5% defence spending target is agreed, defence expenditure could see an increase of $200bn by 2027 (compared to 2024 figures). Even if only the core target of 3.5% is met by 2032, that would still represent over $230bn in additional capital over the next seven years. The spending increases outlined above could represent a permanent shift toward higher baseline defence allocation.

Figure 1: NATO member defence expenditure - 2032 estimates

Source: Macfarlanes analysis using NATO’s data. Assumes an average GDP growth rate for NATO’s European members of 1.55% between 2024 and 2030 based on projections from the International Monetary Fund (IMF) and the Organisation for Economic Co-operation and Development (OECD)

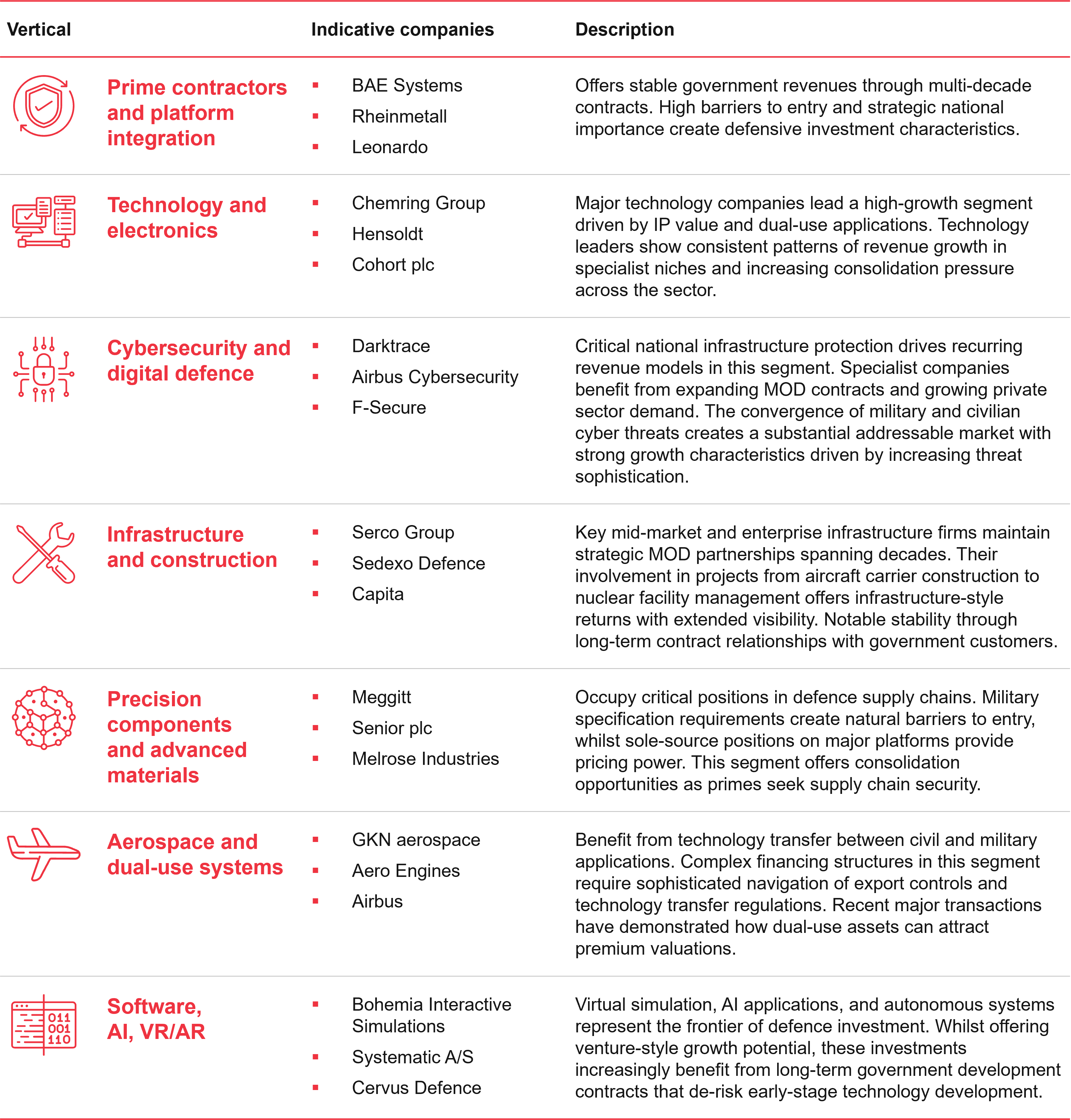

Key verticals in Europe’s defence ecosystem

The substantial spending increases outlined above will flow through Europe's €326bn total addressable defence market24 across distinct investment verticals. Each vertical presents unique opportunities for PCFs and institutional investors to capture this growth, with varying risk-return profiles shaped by regulatory requirements, technical barriers, and government procurement cycles.

We have identified seven key areas where capital deployment can leverage the NATO spending commitments:

Figure 2: Key European defence verticals

European defence companies now occupy 13 of the 15 top-performing positions in global sector indices.25 This outperformance suggests either fundamental repricing of defence sector multiples or a temporary premium that may not be sustained as more capital enters the market. The distinction matters significantly for institutional investors considering strategic allocation versus tactical positioning.

Regulatory clarity has transformed the investment landscape. The FCA's March 2025 statement confirmed sustainable finance rules do not prohibit defence investment.26 Germany went further, explicitly stating that sustainable funds "can of course also invest in companies in the security and defence industry."27

Building strategic positions through European collaboration

The regulatory clarity and spending commitments outlined above create opportunities for institutional investment, but success in European defence markets requires coordination across national boundaries. The diverse ecosystem – spanning protective systems, secure communications, and critical infrastructure – presents investment opportunities across multiple countries and regulatory frameworks.

European market fragmentation historically constrained individual defence contractors but now creates consolidation opportunities across subsystems and components. Technology convergence allows portfolio companies to serve both military and civilian markets, reducing customer concentration while expanding addressable markets.

European sovereignty requirements are creating capability gaps in critical technologies, presenting greenfield opportunities for investors who can structure solutions meeting multiple national requirements. Recent EU-UK defence cooperation progress suggests portfolio companies may be able to access both European Defence Fund programs and UK procurement cycles.

Success depends on identifying investments that capture value across multiple themes rather than isolated opportunities within traditional boundaries. The substantial NATO commitments, combined with regulatory clarity around sustainable investment, suggest strategic positioning in Europe's defence ecosystem can generate attractive returns while supporting broader security requirements.

This article is part of our "rethinking European defence" series: |

Endnotes

- Aviva plc (2025) "Media Statement on Investing in UK Defence" Aviva plc.

- Withers, Iain, and Naomi Rovnick (2025) "UK Investor Legal & General to Buy More Defence Stocks." Reuters.

- ASR Nederland (2025) "A.S.R. Creates an Exception to Invest in the Dutch Defense Industry." ASR Nederland.

- HM Treasury (2025) Spending Review 2025.

- Bow, Michael, and Szu Ping Chan (2025) "Pension Savings to Be Spent on Rearming Britain in Defence Push." The Telegraph.

- Federal Ministry of Defence (2024) National Security and Defence Industry Strategy, Die Bundesregegierung.

- Martin, Tim (2025) EU and UK agree on defense deal, ‘second step’ needed to secure access to $169B in funds, Breaking Defense.

- Stockholm International Peace Research Institute (SIPRI) (2025) "Unprecedented rise in global military expenditure as European and Middle East spending surges,".

- Withers, Iain, and Naomi Rovnick (2025) "UK Investor Legal & General to Buy More Defence Stocks," Reuters.

- European Council (2025) "EU defence in Numbers," 2025; Council of the EU, "SAFE: Council adopts €150 billion boost for joint procurement on European security and defence,".

- Smith, Gary (2025) Germany cuts the debt brakes with defence spending set to soar, Columbia Threadneedle Investments.

- Federal Ministry of Defence (2024) National Security and Defence Industry Strategy, Die Bundesregegierung.

- Serenelli, Luigi (2024) German associations relax exclusion criteria for investment in defence sector, IPE.

- UK Parliament (2025) UK to spend 2.5% of gross domestic product on defence by 2027, House of Commons Library.

- Financial Conduct Authority (2025) "Our Position on Sustainability Regulations and UK Defence." Financial Conduct Authority.

- Khatsenkova, Sophla (2025) Macron’s defence spending plan drives open political divisions in France, Euronews.

- Autorité des marchés financiers (2025) The AMF introduces a fast-track approval procedure for “defence” investment funds.

- Martin, Tim (2024) Norway to double military spending under ‘historic’ long-term defense plan, Breaking Defense.

- Associated Press (2025) Sweden plans largest military buildup since the Cold War amid Russia threat and uncertain US-EU ties.

- Pettersson, Fredrik (2021) Fund savings by sustainability classification, Swedish Investment Fund Association.

- Oleksandra Opanasenko (2025) Finland to increase defense spending to 3% of GDP, Babel.

- Bernacchi, Giulia (2025) Denmark to Boost Defense Spending Beyond 3% of GDP in Two Years, The Defense Post.

- Lunday, Chris (2025) NATO’s Rutte embraces 5 percent defense spending goal, Politico.

- European Council (2025) "EU defence in Numbers," 2025; Council of the EU, "SAFE: Council adopts €150 billion boost for joint procurement on European security and defence,".

- European Council (2025) "EU defence in Numbers," 2025; Council of the EU, "SAFE: Council adopts €150 billion boost for joint procurement on European security and defence,".

- Financial Conduct Authority (2025) "Our Position on Sustainability Regulations and UK Defence".

Federal Ministry of Defence (2024) National Security and Defence Industry Strategy, Die Bundesregegierung.

Authors

Related topics

Like what you are reading?

Stay up to date with our latest insights, events and updates – direct to your inbox.

How can we help you?

Browse our people by name, team or area of focus to find the expert that you need.