/Passle/MediaLibrary/Images/2026-01-09-17-39-34-413-69613d561e42b4e613742f50.jpg)

Proposed clearing threshold changes for EU EMIR and UK EMIR

5 minute read

Who should read this note?

Market participants that (i) are in the EU or UK and trade derivatives, or (ii) trade derivatives with counterparties that are in the EU or UK.

Why does it matter?

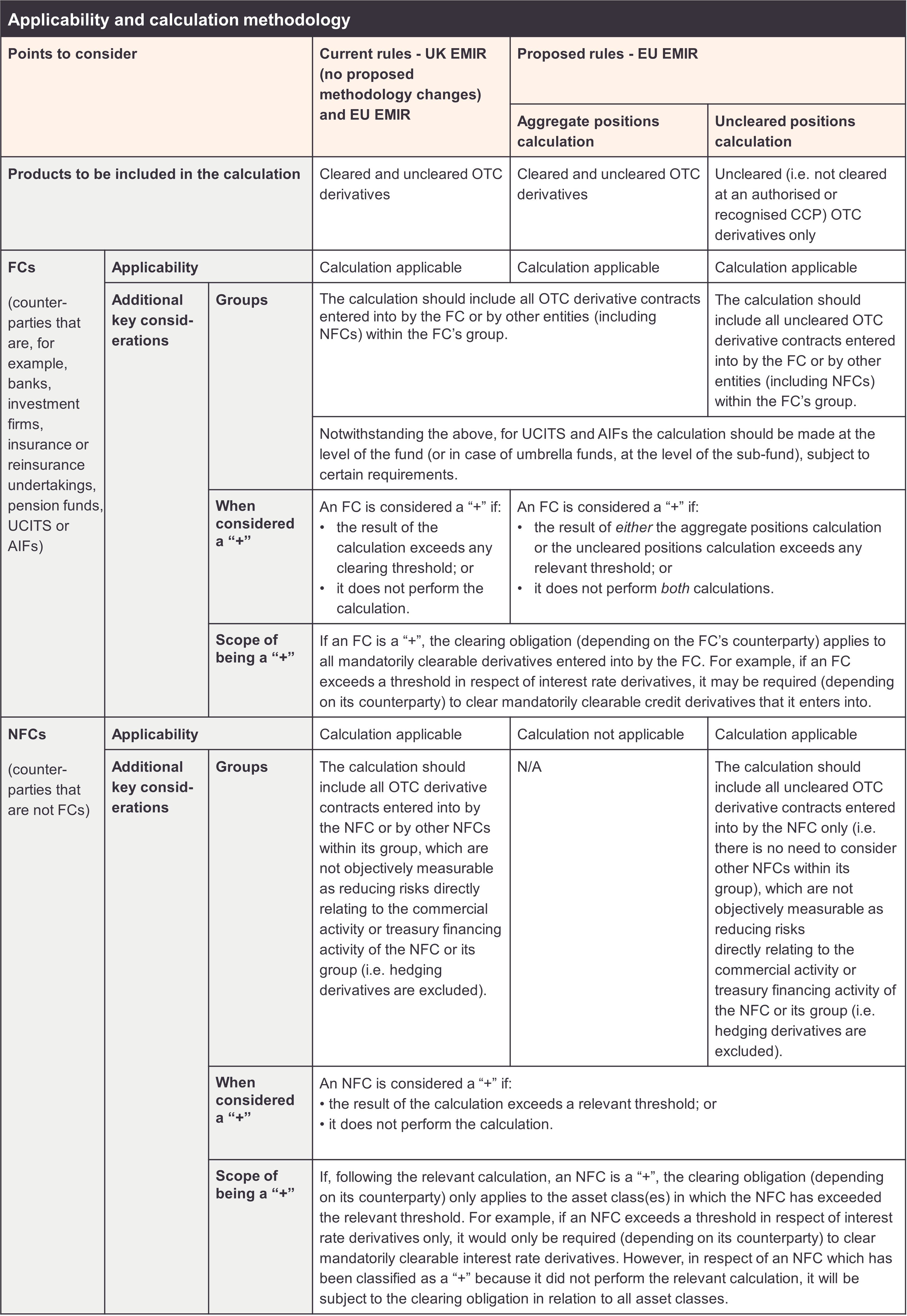

Under EU EMIR and UK EMIR, derivatives counterparties may calculate the notional amount of their trades in order to determine whether they are above or below any of the clearing thresholds (colloquially known as being a “+” or a “-”, respectively). If such a calculation is not undertaken, the entity is considered by default to be a “+”. Market participants that are not in the EU or UK will be required by their EU or UK counterparties to confirm their “+” or “-” status, which may require them to undertake such a calculation also.

Whether an entity is a “+” or a “-” is important to determining the scope of its regulatory obligations (mainly impacting the application of the clearing obligation; but also potentially impacting the requirement for non-financial counterparties (NFCs) to exchange margin).

What are the proposed changes?

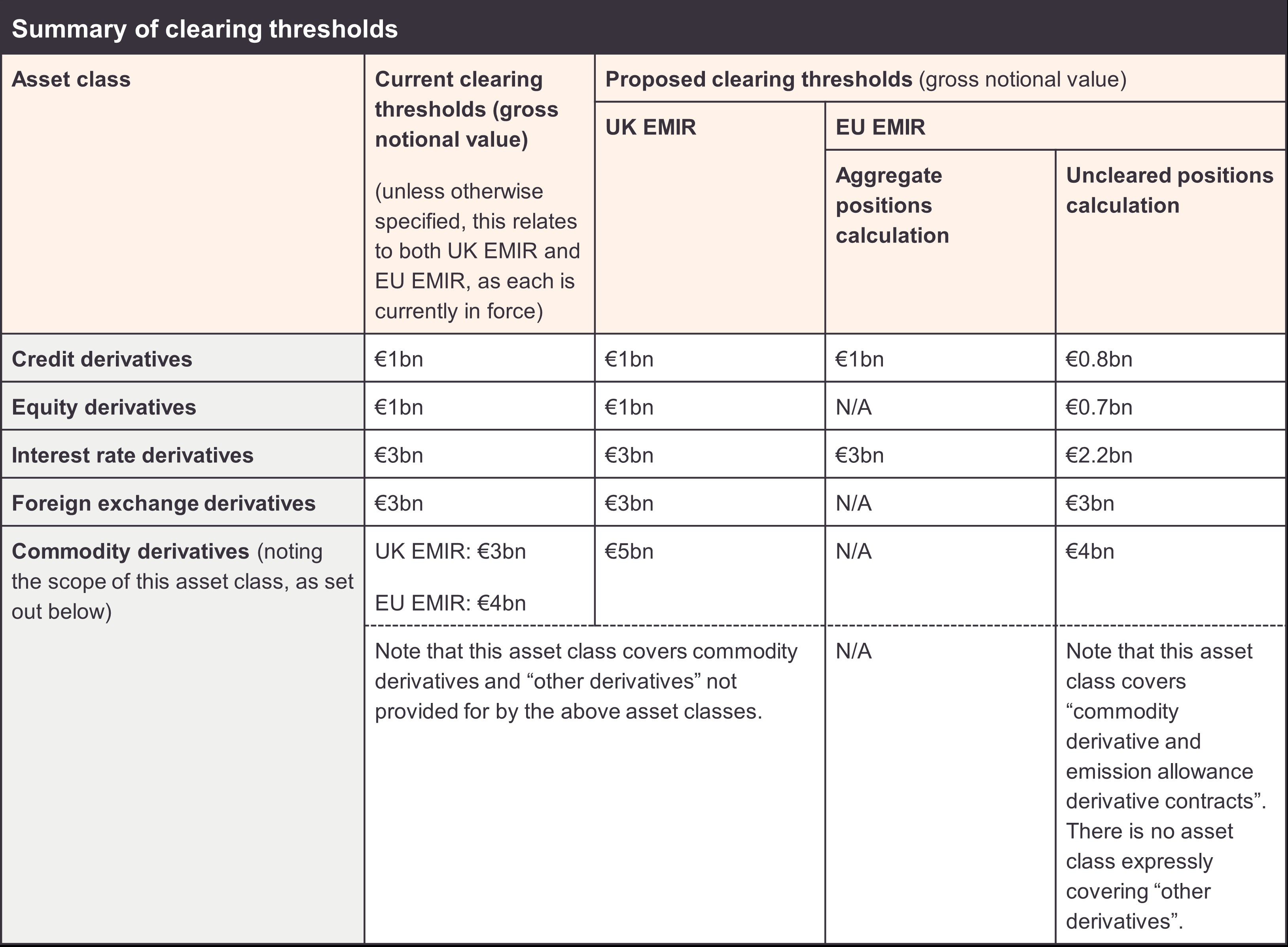

As part of the changes to the EU rules brought in by EMIR 3.0, the clearing thresholds and methodology are being updated. This includes for financial counterparties (FCs), introducing an additional calculation such that there will be two calculations to be undertaken each year – the “aggregate positions” calculation and the “uncleared positions” calculation. The European Securities and Markets Authority (ESMA) has now published its Final Report, which includes the draft amending regulatory technical standards (RTS) setting out its proposed rules.

Separately, the Financial Conduct Authority in the UK has put forward a proposal (in a consultation) to increase the clearing threshold for commodity derivatives under UK EMIR.

We summarise in the table below the current clearing thresholds and each of the proposed changes.

EU EMIR changes

In respect of the proposed EU EMIR clearing threshold changes, we note:

- Timing of calculations: ESMA has helpfully clarified that counterparties have the flexibility to decide whether to recalculate their positions based on the new calculation methodology immediately after the entry into force of the RTS, or to wait until their usual calculation period before applying the new calculation methodology. This should help ensure that the disruption to any existing calculation processes is reduced.

- Reviewing thresholds: As mandated by EMIR 3.0, the RTS also sets out the issues that can trigger a review of the value of the clearing thresholds. This includes significant changes to certain indicators (including (a) the price of the underlying assets; (b) the volatility of the price of the underlying assets; (c) the proportion of OTC derivative transactions that are cleared; (d) the proportion of entities clearing their OTC derivatives transactions; and (e) inflation rates, global financial conditions, and geopolitical and economic policy uncertainties). The indicators should be assessed by EU authorities at least once per year.

- Timing of the RTS: It will still be a number of months before the RTS is (and, therefore, the changes are) in force. ESMA has submitted the draft RTS to the European Commission, who has 3 months to decide whether to adopt the proposed amendments. If the European Commission adopts the RTS, the European Parliament and the Council of the EU have a non-objection period during which they can scrutinise it. Once that has passed (or the European Parliament and the Council of the EU have informed the European Commission that they do not intend to raise any objections), the RTS would be published in the Official Journal of the EU, and would enter into force on the 20th day following such publication.

UK EMIR changes

In respect of the proposed UK EMIR clearing threshold change, we note:

- Timing of the update: The FCA is aiming to make the change to the commodity asset class clearing threshold as soon as possible to address the immediate concerns raised to the FCA by industry and the ongoing fluctuations in commodity prices. The change is being facilitated through a consultation process, and market participants have been invited to comment on the proposal. The deadline for comments in respect of the proposal is 13 April 2026. We would expect the clearing threshold to be updated shortly following the conclusion of the consultation process.

- Wider updates: The change to the commodity asset class clearing threshold is considered by the FCA to be a transitional measure. This is because HM Treasury, with the support of the FCA, is reviewing UK EMIR more generally, including the clearing regime and clearing thresholds. As such, further updates to the UK EMIR clearing regime and clearing thresholds are anticipated in due course.

Market participants should look to understand these proposed changes so that they can be ready to put in place any required processes. When the changes to the clearing thresholds do come into force, there will be some significant differences between EU EMIR and UK EMIR, and market participants that operate under both regimes may need to have in place processes to address both sets of rules.

Please speak to your usual Macfarlanes contact if you have any questions.

Authors

Related topics

Like what you are reading?

Stay up to date with our latest insights, events and updates – direct to your inbox.

How can we help you?

Browse our people by name, team or area of focus to find the expert that you need.