/Passle/MediaLibrary/Images/2026-01-09-17-39-34-658-69613d561e42b4e613742f54.jpg)

Rated note feeders: structuring access to private capital

13 minute read

Note feeder funds are investment vehicles established as part of an existing fund structure.

They repackage an economic exposure to a private capital fund into a debt instrument and by doing so offer a means of accessing the underlying fund other than by way of acquiring an equity interest. This debt instrument is then capable of being rated by a rating agency.

The rise of the rated note feeder fund

Originating in the US, rated note feeder funds were largely designed for US insurers searching for capital solutions that offered better capital treatment of their equity investments. Disincentivised from making direct equity investments into private capital funds due to the higher risk-based capital charges applicable to the holding of equity, when compared to those applicable to the holding of credit assets, insurers looked to rated note feeder funds to secure better capital treatment for their investments into private capital. Elsewhere, in certain Asian jurisdictions (e.g. South Korea), rated note feeder funds have been popular as they provide a means to navigate around some of the onerous approval processes applicable to equity investments which often drive the need for strict debt-only structures in these jurisdictions.

Whilst their origins are niche, the market for rated note feeder funds has gained significant momentum in recent years, and it is reported that in 2025 KBRA alone rated $17bn of note feeder funds, more than double the $8bn of such funds that it rated in 20241. As we move through 2026 there is growing interest in the use of these structures in a Solvency II and Solvency UK context, in particular whether such structures would meet the matching adjustment criteria for inclusion in insurers’ matching adjustment portfolios. The feasibility of these structures in the UK will depend on, amongst other things, whether the notes can be structured to deliver fixed (or, to a limited extent, highly predictable) cashflows that are closely matched with the relevant liabilities.

Rating agencies, such as Fitch Ratings, Moody’s and KBRA, base their ratings of rated note feeder funds primarily on the quality of, and expected cash flows from, the underlying assets of the relevant fund, structural protections within the rated note feeder fund, and the ability of the rated note feeder fund to absorb any losses2. The rating focuses on ensuring the note feeder fund can meet its debt service obligations under the notes.

It is against this backdrop that in this article we unpack the practical and structural considerations that impact both the private credit funds issuing these instruments and the investors that they attract.

What is a rated note feeder and why would you use one?Rated note feeder funds borrow tranching, credit enhancement, structural flexibility, external ratings and cash flow waterfall techniques from the securitisation and CLO markets. They allow investors to access private capital through the purchase of rated debt instruments, (e.g. notes issued by a rated note feeder fund that can, but need not, be combined with an equivalent “day 1” equity interest included in the rated note feeder or the main fund (dual commitment model)). In turn, the rated note feeder fund invests the proceeds of the note issuance into the main fund alongside traditional equity investors. The notes produce cashflows, similar to those from fixed income instruments, and therefore can benefit from a lower risk-based capital factor when compared to a direct equity investment. For institutional investors (e.g. insurance companies, sovereign wealth funds and pension schemes) who are typically subject to more onerous regulatory, accounting and other restrictions than traditional private capital investors, these lower risk-based capital charges are attractive, and for private capital managers these structures facilitate access to a wider pool of capital from alternative sources that might not otherwise be available. Note feeders may be used in other scenarios such as enabling investors to participate in funds which may not be appropriate for them from a tax/accounting structuring perspective e.g. to address the need to own a debt instrument, controlled foreign corporation tax risk or consolidation concerns. In such circumstances, a rating is not normally required. |

Structuring and documentary considerations

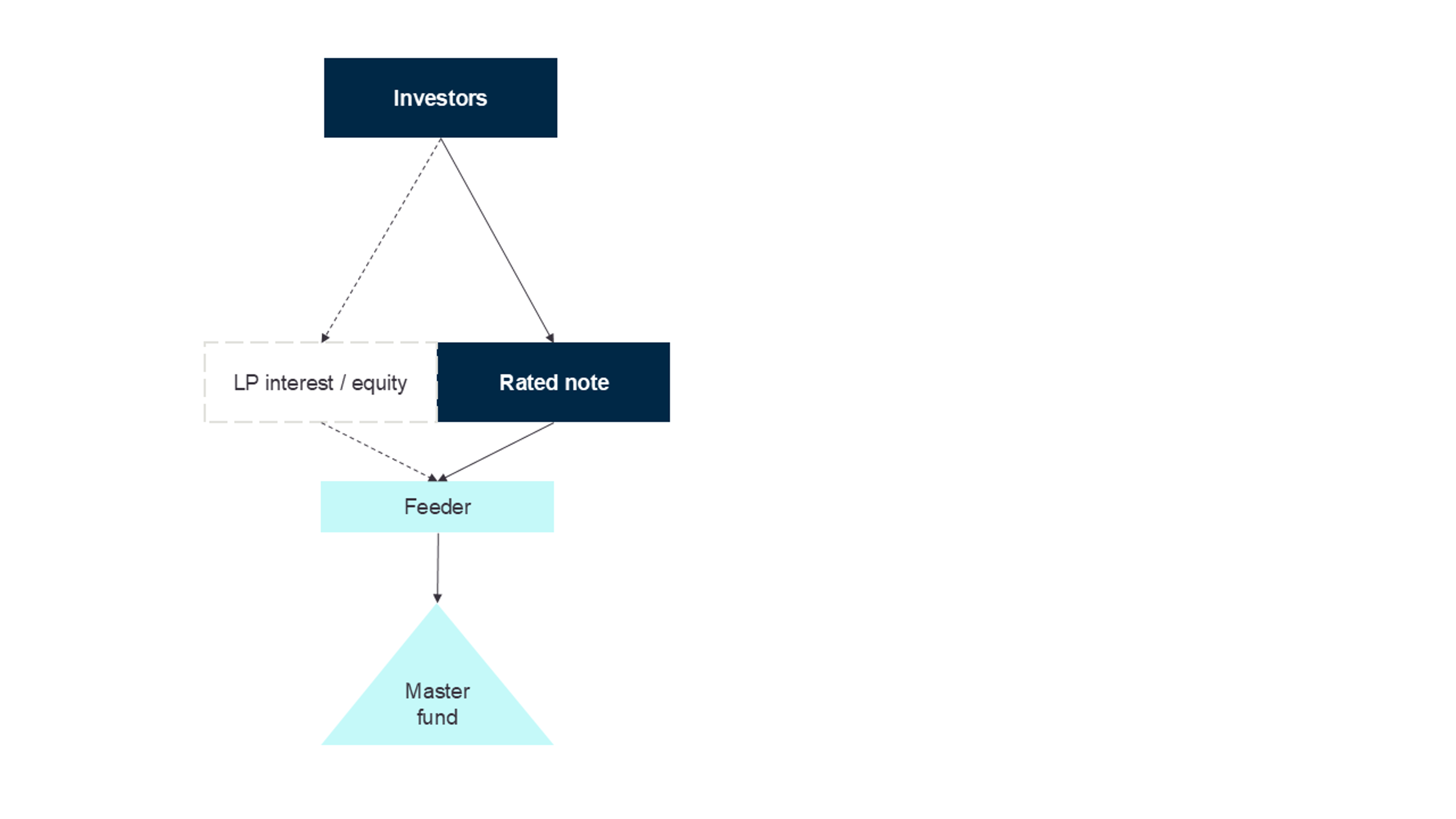

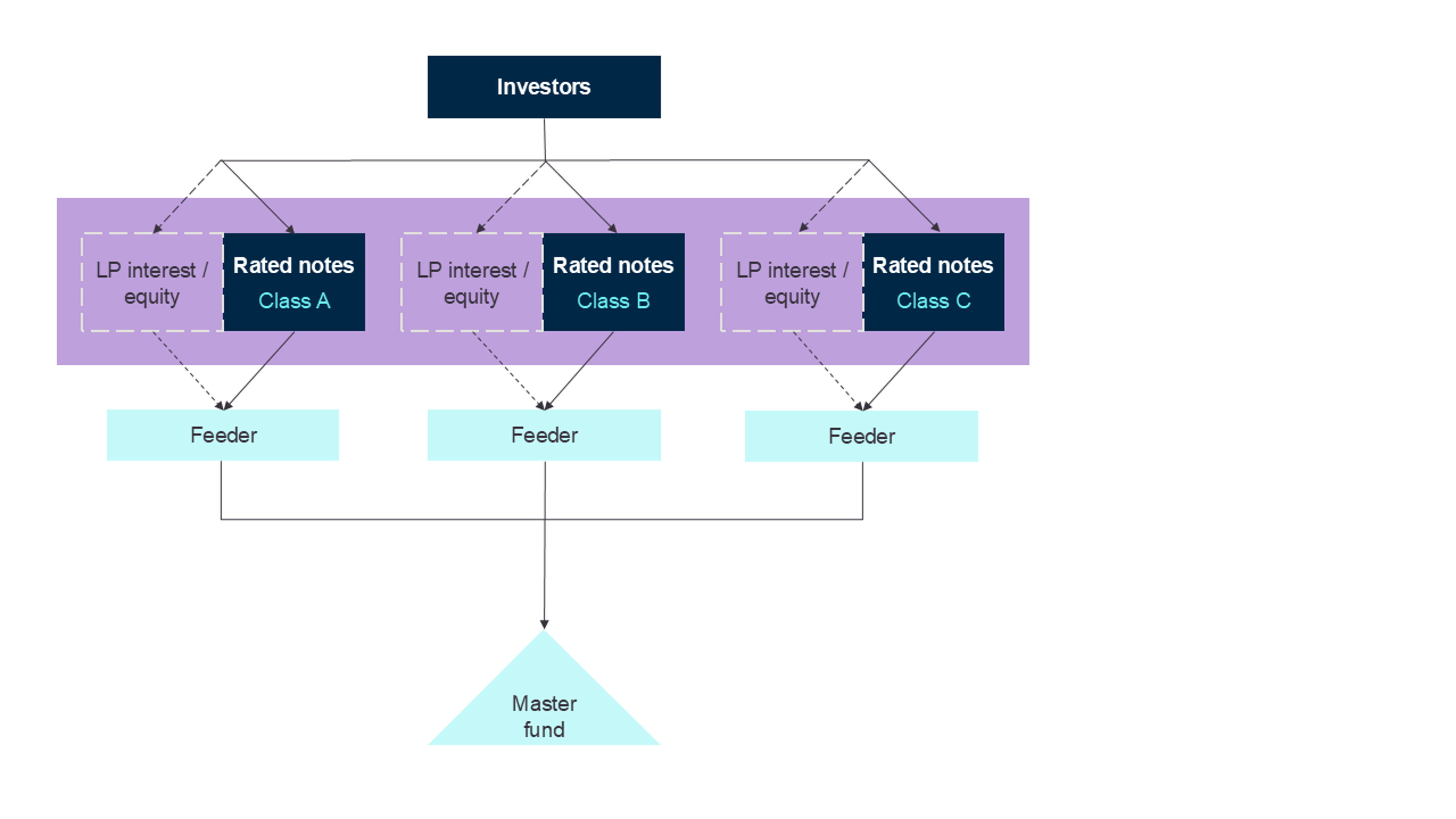

1. Structuring models: one note or two?

There are two principal approaches to structuring a note issuance by a rated note feeder fund: single note structures, where one note is issued at closing with a committed principal amount that is drawn down over time as capital calls are made by the underlying fund (see Figure 1: rated note feeder fund uni-tranche structure); and multiple note (or programme-style) structures, where separate series of notes (which generally rank pari passu with one another) are issued each time the underlying fund makes a capital call, with investors committing to subscribe for new notes at each drawdown (see Figure 2: rated note feeder fund multiple note structure).

The choice between a single note structure and a multiple note structure depends on a range of commercial, regulatory, operational, and investor-specific factors. Applying a broad brush, the single note structure is generally more appropriate where sponsors prioritise simplicity, certainty of commitment, and administrative ease. The multiple note structure is better suited where sponsors value pricing flexibility, capital efficiency, and the ability to reflect actual portfolio composition in each rating assessment.

Figure 1: rated note feeder fund uni-tranche structure

| Note: Equity in the feeder enhances the credit rating. Some rating agencies require it for investment grade ratings. Others rely on the underlying assets and the pooling benefits alone. Consideration needs to be given to any regulatory implications (e.g. securitisation treatment) of this structure if multiple class of notes are issued. |

Figure 2: rated note feeder fund multiple note structure

| Note: Where the rated note feeder fund is structured as a securitisation, the various classes of notes will be ranked and not pari passu. |

2. Separate and independent obligation to call capital

Where, as is most typically the case, rated note feeder funds operate on a dual commitment model, the indenture governing the rated notes often provides that the private capital manager or a lender under a financing to the relevant issuer, can call from investors under either their debt or equity commitment. To facilitate this optionality, it is necessary to ensure there is a separate and independent obligation to call capital in respect of the investors’ fund commitments.

3. Impact of US bankruptcy law

In the current market, rated note feeder funds often rely on underlying assets, master funds, or contractual obligations that are domiciled in the US or governed by New York law. Where this is the case, there is a concern that US debt capital commitments would not be enforceable under the US Bankruptcy Code if the rated note feeder fund were subject to US bankruptcy proceedings. Under the US Bankruptcy Code, if the only trigger for the suspension of debt commitments is the insolvency of the issuer (or an event of default tied to insolvency), then it may be viewed as a circumvention of the ipso facto rule – which renders unenforceable contractual clauses that allow a party to terminate or modify a contract solely because the counterparty has entered into insolvency proceedings - and as a result capital calls blocked.

However, there is no definitive guidance from US bankruptcy courts as to what they view as language circumventing the ipso facto rule. To mitigate this risk, historically some sponsors incorporated a "conversion" mechanic into the note, whereby the noteholders’ commitment starts as a debt commitment before it "converts" to an equity commitment upon the occurrence of an event of default or similar trigger event under the subscription facility. However, it is not established that this conversion approach avoids ipso facto concerns and accordingly rating agencies have been wary of the mechanic and some lenders have objected to it.

For these reasons, the market has increasingly moved towards the dual commitment model, with both a debt and equity interest from “day 1”. And because the capital commitment under the dual commitment model includes an equity component from “day 1”, this approach is not likely to raise ipso facto concerns to the same degree. Practically, in this case it is common for the indenture or note purchase agreement in respect of a fund with a subscription line facility to provide that if an insolvency-related event of default occurs under that subscription line facility, it shall only be possible to call capital under the equity instrument. This ensures that, whilst in the ordinary course of business capital is called as debt, if an insolvency-related event of default occurs, the lender under that facility can rely on capital call under the equity instrument to repay amounts drawn under that facility.

4. Documentation

The sooner documents are sent to the relevant rating agency the better, and participants should ensure that they factor in sufficient time for lender review. Lenders will want to have the opportunity to review and comment on the indenture before it is signed, both in respect of the capital call provisions described above and other bankable provisions, including ensuring that (i) the indenture does not impose any restrictions on guarantees, indebtedness and/or security, (ii) payments under the notes are subordinated to repayments under the credit financing, and (iii) (if required) security is granted over the right to call capital from investors under both the governing law of the rated note feeder fund and, where different, under the governing law of the indenture.

Securitisation considerations

In many ways, the structure of a rated note feeder fund replicates that of a securitisation: it uses an SPV to transform underlying private fund interests into senior rated notes whose returns are dependent on the performance of an underlying pool of assets. These features, coupled with the use of cash flow waterfalls, over-collateralisation, and structural subordination, give these structures all the hallmarks of a securitisation. The question therefore is whether these attributes mean that rated note feeder structures constitute a "securitisation" within the meaning of the applicable EU / UK regulatory framework? And if they do, what does this mean in practice3.

Whether a rated note feeder fund constitutes a securitisation is a highly fact-dependent and technical area and one which requires detailed advice. However where securitisation treatment applies (or is assumed as a matter of prudence), private capital managers will want to consider the practical impact of this on the structure of the rated note feeder fund. Risk retention requirements under applicable securitisation regulation generally require an originator, sponsor, or original lender to retain a material net economic interest of at least 5% in the securitisation, and careful thought must be given to which entity in the structure can satisfy this requirement and on what basis. Where the rated note feeder fund is marketed to EU or UK institutional investors, those investors will themselves be subject to due diligence and ongoing monitoring requirements, meaning that the fund documentation and data infrastructure must facilitate access to underlying asset-level information in the prescribed form and frequency.

Rating agency criteria for securitisations will impose additional requirements around credit enhancement, liquidity reserves, and portfolio eligibility criteria, and these will need to be considered alongside regulatory transparency and reporting obligations to avoid duplication or inconsistency. On the upside, classification of a rated note feeder fund as a securitisation affords a more efficient capital adequacy treatment for institutional investors (e.g. insurers) (For more information read Insurers and the EU securitisation reforms: an asset class finally unlocked?).

Interaction with evergreen products

One increasingly popular application of rated note feeder structures is their deployment alongside evergreen and semi-liquid fund products to open these products to a broader investor base, specifically institutional investors. A growing number of private capital managers have utilised rated note feeder structures in connection with their evergreen private credit offerings, and the market for these products continues to grow4. Evergreen private credit funds are well suited to rated note feeders because the underlying assets are debt-related and produce regular income. This supports the coupon payments on the rated notes and makes the structure more amenable to credit analysis by the rating agencies.

Tax considerations

Private capital managers and investors alike will need to consider the tax implications of establishing a feeder fund in a particular jurisdiction. Jurisdictions that are widely considered to be LP-friendly include Jersey, Luxembourg, the Cayman Islands and Ireland. Depending on the jurisdiction selected, there may be more onerous disclosure and transparency, risk retention and due diligence requirements to be satisfied.

Operational impact of the use of rated note feeders

The documents governing rated note feeders are more akin to those papering similar debt instruments than traditional fund documentation and will often incorporate standard noteholder covenants, events of default and information undertakings, and provide for the appointment of registrars and trustees. They offer flexibility in terms of interest payments and waterfall mechanics, and this can be used to mirror the terms of the underlying fund documents, and therefore enable private capital managers to continue with their existing reporting arrangements and the mechanics with which they are familiar for management of the fund structure as a whole. There are likely to be additional obligations regarding service provider arrangements given the rated notes may require a registrar to be appointed or, in the event the notes are listed, private capital managers will need to be familiar with how to comply with their ongoing obligations with the exchange.

For investors, there are limited operational differences between investment in a rated note feeder fund and an equity investment in a more commonly-used fund vehicle, but investors can expect to see variation in the onboarding process and ongoing reporting given the distinct nature of the notes. Investors will likely subscribe for notes by entering a commitment letter, note purchase agreement or similar and will receive their return by way of fixed and variable interest payments which may impact their internal tax and accounting processes.

Rating considerations

Investors do not always require a note feeder to be rated if they are able to assess the risk profile of the entity internally, but it can be appealing as the rating offers an extra layer of security for investors. Indeed, whilst ratings do not come cheap and obtaining a rating for a rated note feeder fund can involve meaningful incremental costs relative to traditional fund structures (e.g., upfront rating agency fees, ongoing surveillance fees, legal costs, and administrative expenses), the favourable regulatory capital treatment and attractive yield unlocked by a rating generally are, if the amount of capital raised is sufficient, widely considered to justify the expense.

Whilst securing a rating adds an extra step to timelines and often requires additional resource and coordination from issuers and their sponsors, (e.g. coordination with the rating agency on the initial rating assignment and ongoing affirmations, preparation of documentation (including note purchase agreements or indentures), ensuring that the transaction structure meets ratings agency requirements around subordination, credit enhancements, and payment priority, and analysis of potential accounting consolidation issues) it is a more than manageable process for sponsors who engage experienced advisers and begin coordination with rating agencies and lenders at an early stage.

The outlook

The attraction of rated note feeder funds is clear: for private capital managers, these products offer a means to access a broader and more diversified investor base at a time when competition for institutional capital is growing. For investors, rated note feeder funds offer a route into private capital that is more aligned with their regulatory and operational frameworks than a direct equity commitment.

As these demands grow and provided that participants continue to approach these structures with the rigour and early engagement that they demand, rated note feeder funds are expected to rapidly move from a niche capital-raising tool to a standard feature of the private capital toolkit. That said, this remains a space in which private capital managers and investors alike will be conscious to carefully navigate the impact of applicable securitisation regulations, US bankruptcy considerations, tax structuring and maturing rating agency criteria. This complexity of interlocking requirements underscores the importance of specialist advice and cross-disciplinary coordination from the outset.

Footnotes

1 Financial Times (2026), The black-box funds fuelling insurers' private credit binge, 20 March 2026

3 It is worth noting that where there are no EU or UK investors, sponsors may be able to structure around the requirement to comply with the EU and UK securitisation regimes altogether. For example, by establishing the issuer SPV in an offshore jurisdiction such as the Cayman Islands, thereby falling outside the territorial scope of those regimes.

4 KBRA alone had assigned ratings to seven feeder fund transactions investing in evergreen master funds, representing $2.1bn in combined debt and equity commitments. KBRA (2025), KBRA releases research - Private Credit: Maturity Matching - Rated Notes and Evergreen Funds, 13 May 2025.

Authors

Related topics

Like what you are reading?

Stay up to date with our latest insights, events and updates – direct to your inbox.

How can we help you?

Browse our people by name, team or area of focus to find the expert that you need.