/Passle/MediaLibrary/Images/2026-01-09-17-39-34-159-69613d56ed0bb2914998086c.jpg)

Co-investment in private credit: structuring and fee considerations for sponsors

12 minute read

As private credit has matured, investor demand for co-investment opportunities has increased significantly and co-investment has become part of the product architecture rather than merely an ancillary relationship benefit1.

There is no single driver for this trend, but typically a combination of investors seeking: (1) enhanced returns, through access to individual credits on a reduced- or no-fee basis; (2) greater control over portfolio construction, through the ability to tilt exposure toward preferred sectors, geographies or risk profiles; and/or (3) stronger relationships with their sponsors and a better understanding of their origination, underwriting and monitoring processes.

Co-investment has long been a staple of private equity, with the industry coalescing around a relatively standard structure that is well understood by sponsors and investors alike: co-investing investors invest in a sponsor-controlled SPV ((Special Purpose Vehicle) - typically a limited partnership) that then invests in a single underlying portfolio company alongside the flagship fund.

The different dynamics typical in private credit – a larger number of investments and more compressed investment decision-making timeframes – result in both sponsors and investors looking for alternatives to the classic PE-style single asset co-investment SPV. Before selecting a structure, sponsors should be clear about what opportunity the co-investment programme is intended to solve for. In credit, the structuring choice is usually driven by five variables:

- whether the investor requires lender-of-record status;

- the degree of execution certainty required within compressed deal timelines;

- the number and sophistication of co-investors;

- the sponsor’s intended fee, carry and other economics; and

- the regulatory, tax and operational footprint of the structure.

The same investor demand may therefore point to very different legal architecture depending on whether the sponsor is seeking committed overage capital, a relationship-driven deal-by-deal allocation process, or a purely economic risk transfer. This article considers some of those alternatives from the sponsor’s perspective including their advantages and disadvantages.

For the purposes of simplicity, we have not depicted in the diagrams below the detailed structure of a typical flagship fund, co-investment vehicle or SMA which often will comprise multiple vehicles (e.g. currency feeders and blockers). In addition, in the context of a typical private credit fund structure, it is very common for the fund/SMA vehicle to have a corporate asset holding company (an “asset holdco”) as a subsidiary of the fund through which investments are held.

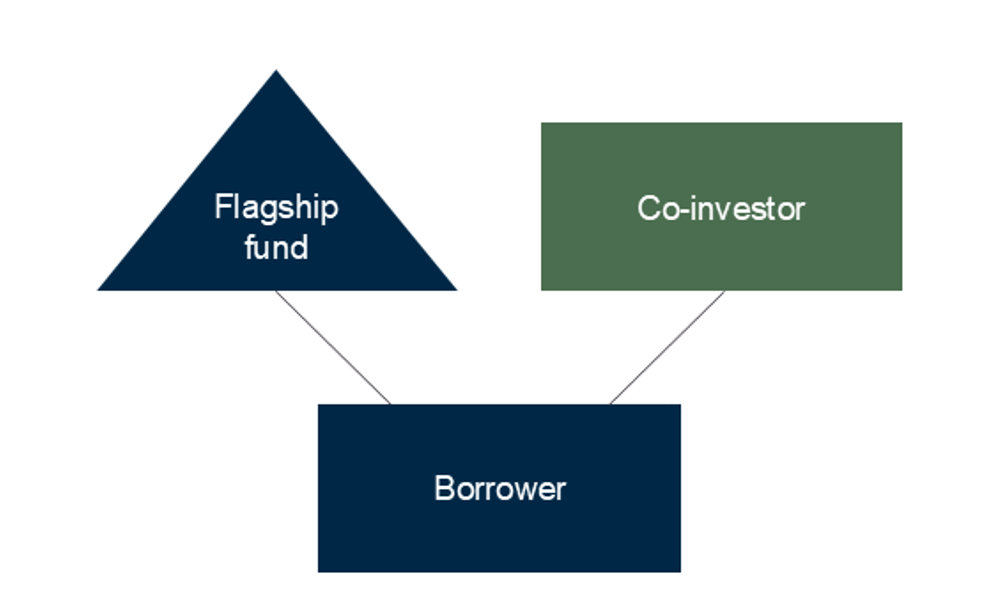

1. Direct co-investment

With this alternative, the co-investor effectively acts as a parallel lender of record under the same syndicated-form credit agreement as the sponsor’s flagship fund (and any other accounts – e.g. SMAs – managed by the sponsor).

This is the least common of the structures we encounter; typically, because it puts the ongoing deal decision-making onus directly on the co-investor and beyond the sponsor’s control, which is unappealing for the sponsor and burdensome for the co-investor, and the difficulty the structure provides in structuring profit sharing between the sponsor and the co-investor.

Direct co-investment advantages

Accesses certain pools of capital which require lender of record status.

Fewer house entities and, therefore, less cost and operational complexity of running them.

Direct co-investment disadvantages

More complexities with borrower interactions, with voting rights vesting directly in – and requiring the active engagement of – the co-investor. This is potentially operationally burdensome as the co-investor either seeks, or is required, to be more involved in the day-to-day management of the loan.

Increases deal execution issues, particularly in respect of withholding tax treatment if the co-investors do not have vehicles established in jurisdictions with favourable treaties vis-à-vis the borrower jurisdictions. Similar complications will also arise if the deal comprises “equity-kicker” elements.

For the same reasons, it becomes harder to create standard documentary positions, as certain elements need to be tailored for the particular blend of participating entities.

Co-investors may need to run their own approval committee processes to invest in their own name, adding more steps and potentially lengthening execution timetables.

Transfers of positions may require borrower consent as the sponsor and co-investor will not fall within typical affiliate and related fund exemptions to assignment and transfer restrictions.

From a tax perspective, this option is relatively straightforward as there is no need for the sponsor to establish any bespoke vehicle for the purposes of the co-investment and consider the tax treatment and attributes of the vehicle. However, as mentioned above, it requires the investor to bring their own “exemption” (be it treaty or otherwise) where the underlying investment is in a jurisdiction which has interest withholding tax. In addition, the co-investors will be directly responsible for their own investment-related tax compliance aspects (e.g. completion of procedural formalities to access relief) which may not be desirable.

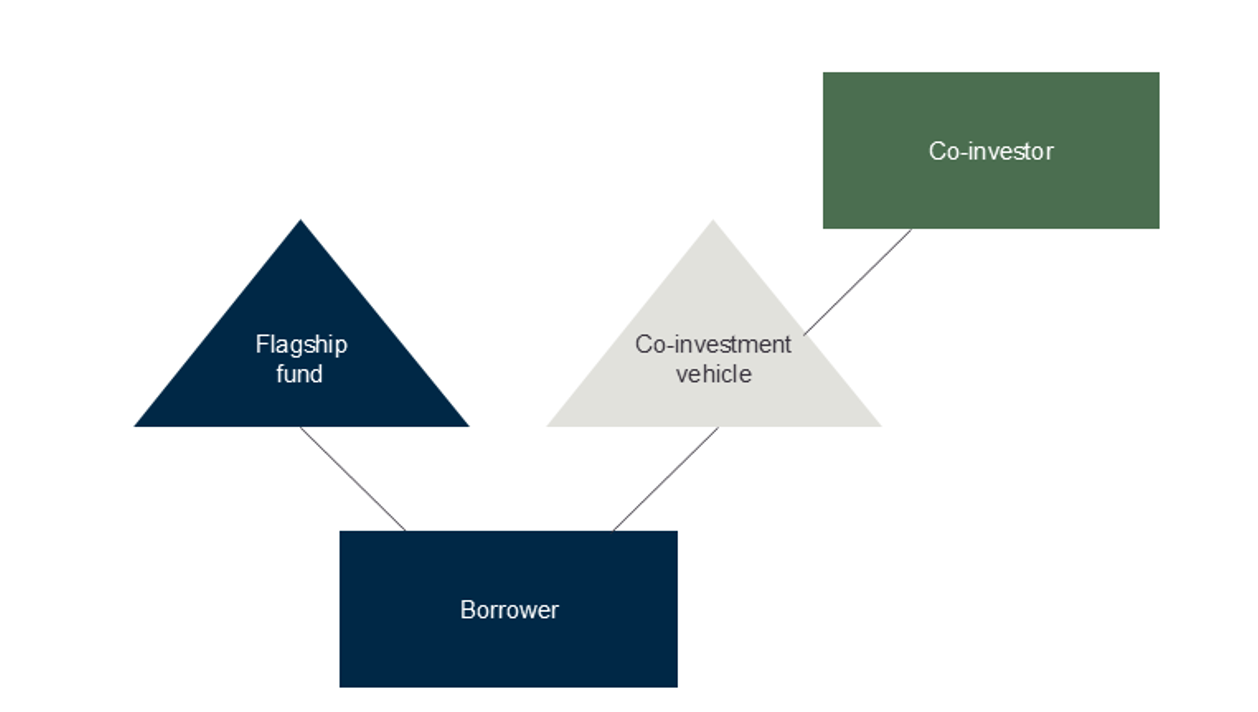

2. Dedicated blind pool co-investment vehicles (sidecars)

Building off the favoured private equity model of establishing a single asset co-investment SPV at the time of the co-investment transaction, this option involves the sponsor forming a dedicated sidecar vehicle at substantially the same time as the flagship fund. Investors who commit to the flagship fund will have the option of committing to the sidecar, and capital committed to the sidecar will then be available to the sponsor to deploy in co-investment opportunities alongside the flagship fund, as and when they arise.

The terms of sidecar vehicles can vary significantly – some give the sponsor full discretion to deploy committed sidecar capital; others give participating investors opt-in or opt-out rights – although typically sidecars will offer lower or no fees and carry.

The key driver is to encourage greater investment in the flagship fund. Investors only get access to the co-investment vehicle if they have committed to the flagship fund. Some sponsors require investors to write a certain size cheque to the flagship fund to get access; others keep it entirely discretionary.

We have seen limited examples whereby the sponsor has structured this through the flagship fund. However, unless it is a compartmentalised vehicle, those investors who are not participating may struggle to get comfortable with the potential cross-contamination of such co-investments with the flagship fund investments.

Dedicated blind pool co-investment vehicles (sidecars) advantages

Can provide the sponsor contractual comfort as to the capital available for deployment in excess of that raised in the flagship fund.

Reduced interaction and due diligence with co-investors and therefore quickens the deal execution process.

Assuming the investor has limited ability to opt out, or has to opt out quickly, provides execution certainty and the ability to meet compressed deal timeframes.

May encourage commitments to the flagship fund to access a blended management fee rate and carried interest percentage.

Leaves decision-making and voting in relation to the underlying transactions with a sponsor-managed vehicle which ensures consistency of voting positions and reduces operational requirements on consent requests. This is particularly important in restructuring or enforcement situations.

Dedicated blind pool co-investment vehicles (sidecars) disadvantages

Setting up a dedicated co-investment vehicle is likely to raise questions from investors as to why the sponsor requires so much additional capital – is the sponsor targeting investments that are too big for the fund and its proposed investment strategy?

There is a cost to setting up the vehicle in advance; especially if there is no guarantee the sponsor will find co-investments to offer it.

Intra-life, imposes a greater operational burden, and associated cost, of managing additional vehicles.

Investors need to ensure they have the capital available to invest when the co-investment vehicle calls for it, even though that may never happen. This can lead to a cash drag for investors which might make them hesitant to participate.

Investors are likely to still want some control over the investments they get exposure to. If there are a number of investors opting out of co-investments, this can undermine the very nature of having the vehicle (i.e., guaranteed co-investment capital).

From a tax perspective, the expectation would be that the sidecar structure mirrors the asset holdco structure of the flagship fund (e.g. if the flagship fund is a Luxembourg partnership with a Luxembourg company as the holding company, we would expect the co-investment vehicle to mirror that structure). However, there might be some flexibility on timing and the asset holdco under the co-investment vehicle could be set up prior to the first deal. Depending on the type of asset holdco used, there may be additional structuring considerations, for instance if the flagship fund uses a UK qualifying asset holding company as their asset holdco, whether the co-investment vehicle can use a similar asset holding company will depend on whether the conditions (including the ownership conditions) of the UK qualifying asset holding company regime are met.

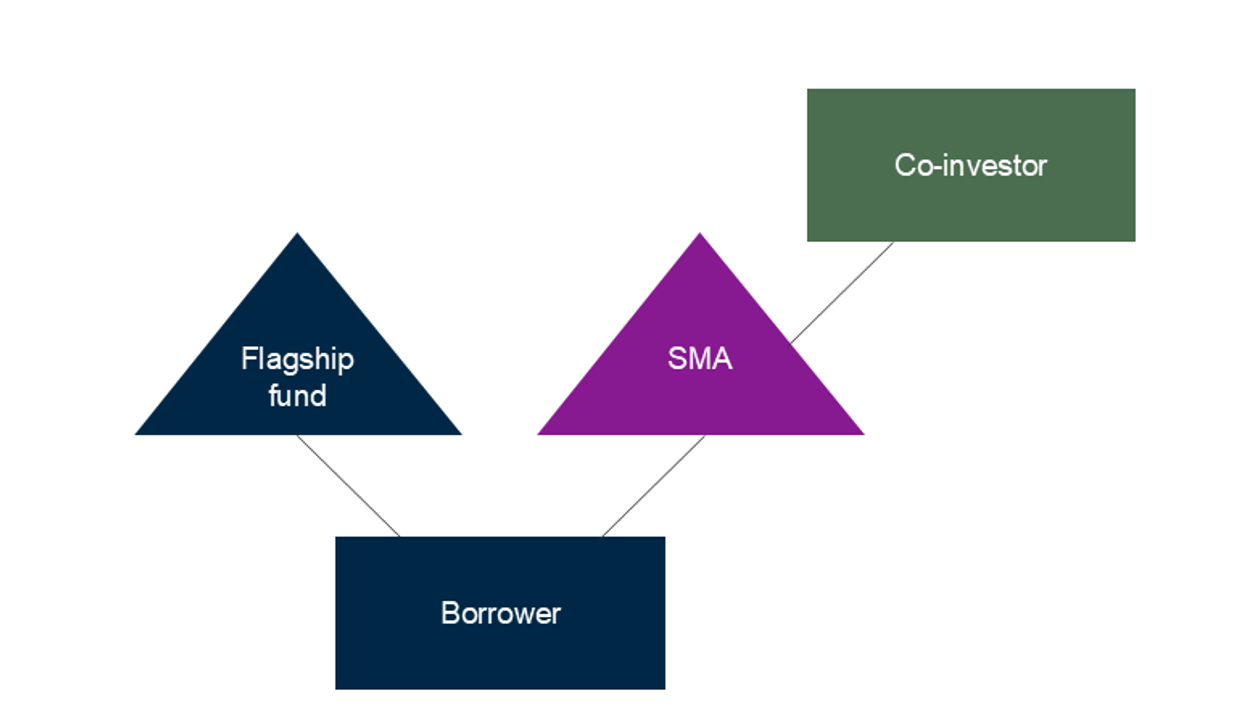

3. SMAs

Some sponsors limit co-investment access to their SMAs – bespoke investment programmes agreed with significant investors. When an SMA’s investment parameters overlap with those of the sponsor’s flagship fund(s), the SMA and the fund(s) will invest alongside each other in accordance with the sponsor’s agreed investment allocation policy.

An SMA’s ability to access co-investment can either be given at the sponsor’s full discretion or with the SMA investor having an opt-in or opt-out right. It also may either be a dedicated SMA for co-investment only or an allocation to co-investment above and beyond their SMA commitment.

SMA advantages and disadvantages

The same advantages and disadvantages set out in section 2 (Dedicated blind pool co-investment vehicles) apply and in many scenarios we would see an SMA co-investing alongside either a dedicated blind pool co-investment vehicle (section 2) or deal-by-deal co-investment vehicles. However, one particular advantage is that this structure affords the participating investor access to co-invest across different funds of the same sponsor (whether different vintages of the same flagship strategy or differentiated strategies under a single sponsor umbrella) without requiring specific vehicles for each. This reduces the cost and administration burden flagged as a disadvantage in section 2 above.

From a tax perspective, the same considerations set out in section 2 above apply, albeit that the SMA would typically be an existing structure with its own asset holdco and as such should be generally able to invest alongside the flagship funds which aligns with the strategy it is pursuing.

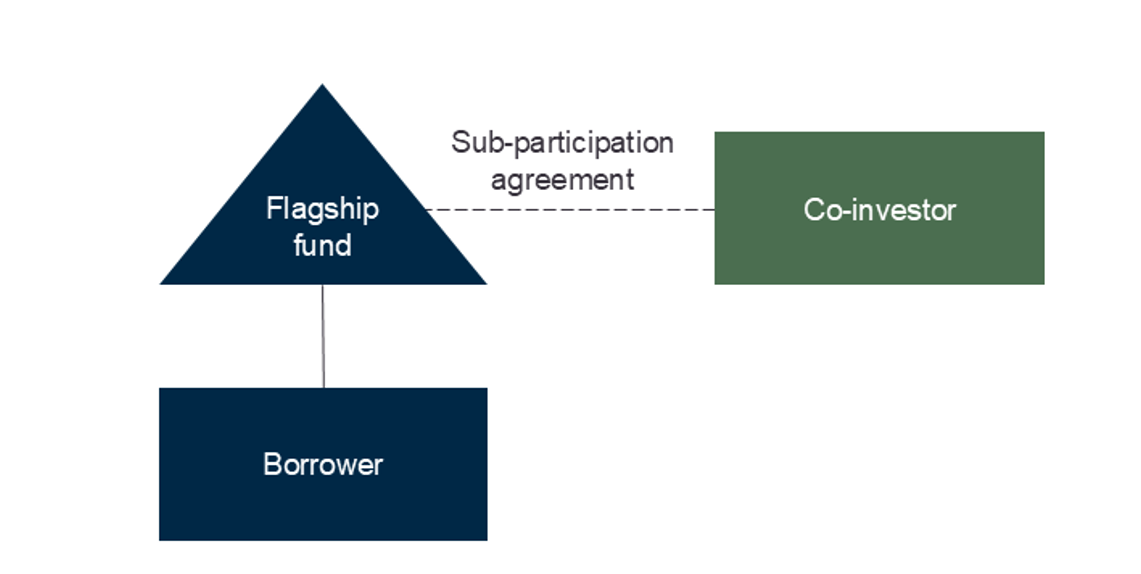

4. Sub-participation

A contractual alternative, this involves the flagship fund being the (sole) lender of record with the underlying borrower and entering into a sub-participation agreement in respect of that position with the co-investor that transfers a portion of the fund’s economic risk to the co-investor without changing the underlying credit agreement. The fund remains the lender of record but economics and returns are passed to the co-investor before they hit the flagship fund vehicles.

Sub-participation advantages

- One lender of record resulting in less operational complexity.

- No need to establish and operate additional vehicles.

- Control and interaction with the borrower remains solely with the sponsor. But the sub-participation agreement can be tailored to include derivative enshrined rights as agreed between the sponsor and the co-investor on a case-by-case basis, providing flexibility.

- Confidentiality - sub-participants are potentially unknown to the borrower, though loan documentation is becoming more sophisticated on this point with lenders of record increasingly being required to disclose sub-participations to the underlying borrower. There is frequently a distinction made between voting and non-voting sub-participations, with borrowers significantly more sensitive to the latter (i.e. they are focussed on who controls decision-making with respect to their debt).

Sub-participation disadvantages

- No direct recourse for the co-investor to the underlying borrower and the loan’s security package. They are wholly-reliant on the sponsor.

- As above, loan documentation is becoming increasingly sophisticated in regulating sub-participations alongside lender transfers, imposing the same borrower consent requirements unless the co-investor fits in an exempted category (most likely as a white list lender, though they do not commonly include investor entities, comprising banks and credit funds – that is gradually changing as more investors participate directly in private credit).

- Sub-participant co-investor takes on the credit and insolvency risk of both the flagship fund (which is a pooled investment vehicle) and the underlying borrower.

This option is potentially the most involved from a tax perspective as the tax treatment of sub-participation can be complex depending on the structure and jurisdiction of the investment. The key points to consider would include the deductibility of the sub-participation payments for investors, withholding tax on sub-participation payments (usually not an issue) and whether the arrangements would impact the tax treatment of the underlying investment (e.g. whether the recipient of the interest is still considered to be the beneficial owner of that interest taking into account the sub-participation agreement).

Structuring – a tailored approach

Ultimately, the optimal co-investment structure for a given sponsor and its investors will depend, to a significant extent, on tax considerations and the degree of control needed by investors. Other factors include deal size, borrower preferences and documentary references, the number of co-investors and – at both sponsor and investor level – internal resource and infrastructure.

Finally, consideration needs to be given to the implication of AIFMD II on the proposed structure. For example, relevant questions are likely to include whether the arrangement constitutes a transfer, whether the 5% risk-retention requirement is engaged and whether the structure could be characterised as a loan-to-distribute strategy. AIFMD II is evolving as it is implemented and needs applying on a case-by-case basis.

Beyond the structuring – fee models

Historically, private equity co-investment was offered management fee and carry free. This was the initial basis on which investors sought co-investment opportunities in private credit. However, as management fee rates and carried interest percentages are lower in private credit, we have seen a divergence from the management fee and carry free model and sponsors thinking more creatively. For example:

- An upfront administration fee (akin to a one-time management fee). For certain investors who cannot pay management fees on their co-investment this can be a useful alternative structure.

- A ratcheted carried interest which is dependent on investment in other products of the sponsor. For example, full fees and carried interest are charged on the co-investment until the investor has invested a certain cheque size in other full fee-paying products.

- A ratcheted fee and carried interest based on number of, or quantum of capital deployed into, co-investments. For example, the first three co-investment opportunities are fee and carry free and then full fees and carry are paid on subsequent co-investments.

- The sponsor retains the co-investment’s pro rata share of other fee income (such as arrangement, monitoring, board, syndication or amendment fees) rather than applying that amount as an offset against the management fee, as would typically be the case for the flagship fund’s pro rata share.

It ultimately depends on the negotiation power of the investor and the underlying asset. As was seen recently2 in private equity with the significant capital inflows from retail capital, sponsors may not need to continue offering reduced fees on co-investment to institutional capital as they can offer it on full fees to retail capital. The impact of retail on co-investment in credit though is yet to be seen.

Footnotes

1 AIMA/ACC report Trends in private credit fund structuring 2025: “in 2023, about 70% of respondents anticipated increasing demand for co-investments, with this rising to 92% of respondents in 2025”. Private Debt Investor in 2025 reported: “50% of investors had intentions of participating in private credit co-investment opportunities in the prior 12 months”.

Authors

Related topics

Like what you are reading?

Stay up to date with our latest insights, events and updates – direct to your inbox.

How can we help you?

Browse our people by name, team or area of focus to find the expert that you need.