/Passle/MediaLibrary/Images/2026-01-09-17-39-33-816-69613d55d42b6e4a58415606.jpg)

The Bank of England’s private capital SWES test – a blueprint for global regulators?

9 minute read

As private credit plays an increasing role in the financial system, its rapid growth, tighter credit conditions and the heightened geopolitical risk have combined to put the sector under the spotlight which may prompt close supervision from regulators in the UK and globally.

In that context, the Bank of England’s (BoE) system-wide exploratory scenario (SWES) exercise is being closely watched as a key indicator for how global regulators may assess, and potentially seek to regulate, the risks associated with private credit.

What is the Bank of England SWES exercise?

The BoE private market SWES exercise is seen as unique. Unlike traditional stress tests that focus primarily on the banking sector, this SWES exercise takes a broader view by examining how a wide range of financial market participants behave collectively during periods of severe market stress. A similar exercise was undertaken in 2023 which focused on the gilt market, but this is the first of its kind to investigate private markets.

The primary objective of the exercise is to understand how different types of financial institutions respond to a major global economic shock scenario. Through the exercise the BoE will explore how liquidity demands and risk management actions may interact across the financial system and extrapolate that collective behaviour to see whether it poses a systemic risk to the economy.

“Leverage is a layer cake – at the borrower, fund and sponsor level – making it hard to measure. Loans are sometimes sliced and diced into CLOs and often held or distributed on the basis of ratings agency assessments. And complex connections to the rest of the financial system, including banks, insurers and reinsurers, create an ecosystem where losses that are already hard to size become even harder to trace.” Sarah Breedon, Deputy Governor, Bank of England (April 2026) |

One of the principal concerns from the BoE is understanding the level of connectedness between the different participants in the private market eco-system. The BoE’s interest arises because banks participate in private markets through various channels.

The participants are asked to respond to a hypothetical but severe global market stress scenario involving significant shocks to the economy. The focus is not on whether individual firms survive the stress, but rather on understanding how their actions collectively - such as selling assets, calling for collateral, or reducing exposures - might propagate and amplify the initial shock.

The participants1 draw together private capital managers, banks and institutional investors from across the financial system.

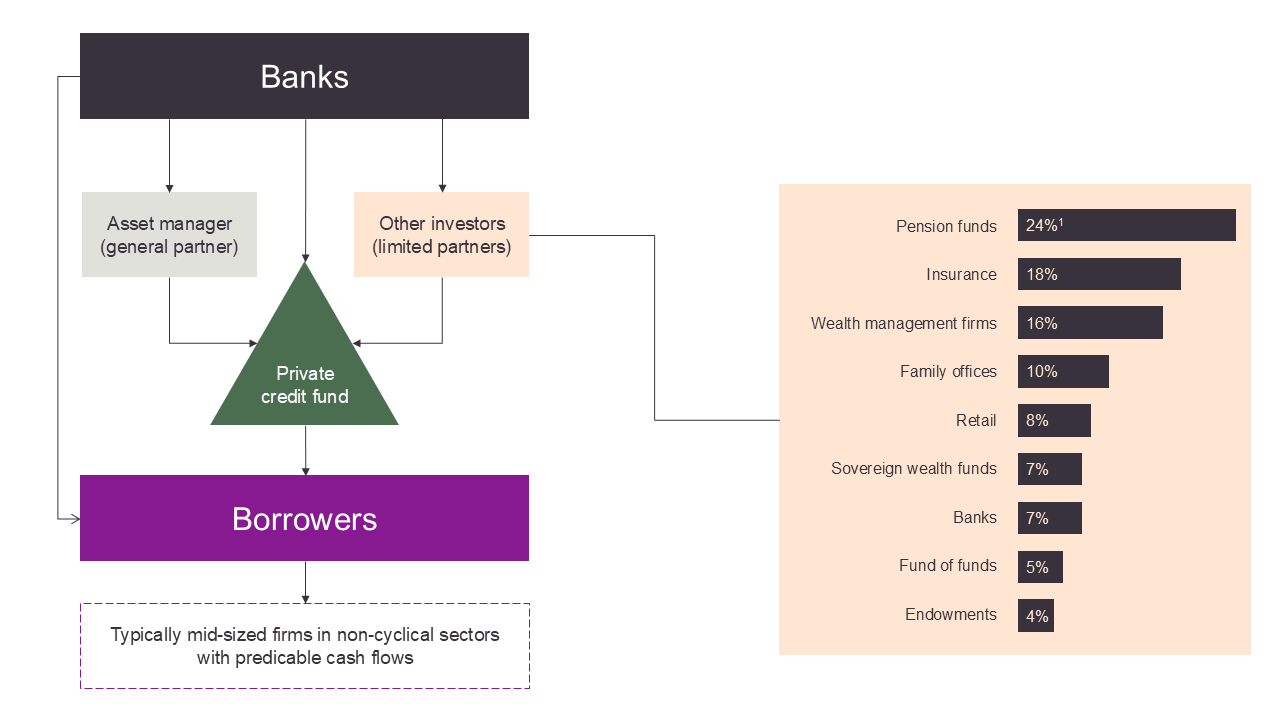

Figure 1: private credit interconnectedness and allocations by investor type

Source: AIMA: Allocations to private credit by investor type in 2024, Financing the Economy 2025

Some 45 market participants in total have agreed to be involved in the exercise on a voluntary basis. Those outside of the exercise should monitor the findings as it is likely to indicate the future direction of regulation.

What are the key areas of focus?

1. Liquidity mismatch

One of the primary concerns for regulators is the potential for liquidity mismatches, whereby investors are offered regular redemption rights from fund structures whilst the underlying assets remain invested in illiquid investments. Private credit funds are traditionally closed-ended and offer a fundamentally different proposition from retail-orientated funds in terms of subscription and redemption frequency, liquidity and life cycle. In this regard, a recent publication by the European Central Bank provided some reassurance that regulators were able to draw a distinction between the different fund types and the different risks they posed, noting that "liquidity mismatch in private credit funds appears limited in traditional closed-ended private credit funds".

That said, the continued growth in private credit is expected to be bolstered further by the expansion of evergreen fund structures. To manage liquidity, these types of funds typically include some liquidity in their portfolio, rely on robust governance and liquidity management frameworks and employ a range of liquidity management tools, such as redemption limits, notice periods and dilution adjustment. These measures are specifically designed to address liquidity mismatch concerns. In the European Union, revised and enhanced rules on liquidity management for credit funds have been introduced through the AIFMD II reforms, with open-ended loan origination funds required to demonstrate to national regulators that their liquidity risk management system is fit for purpose, and a mandatory requirement to select at least two liquidity management tools from a prescribed list. It is certainly possible that other global regulators in this space may seek to introduce similar specific requirements on liquidity management.

2. Transparency and data gaps

A recurring theme is the concern that regulators lack sufficient data to monitor private credit effectively, creating an environment in which they feel unable to quantify the market or assess its risks with confidence. The Financial Stability Board (FSB) has identified four key challenges in this regard, which may signal the areas where local authorities choose to impose additional data requirements.

- The FSB highlighted limited data at both fund and investment level, making it difficult to identify and quantify private credit within the broader financial system.

- It noted unclear and inconsistent identifiers for underlying financial instruments and borrowers, resulting in insufficient granularity of exposures.

- It identified an inability to assess risks arising from multi-layered investment structures, including the use of leverage within those structures, thereby obscuring indirect exposures.

- It highlighted an overall lack of comprehensive reporting on leverage, limiting regulators' capacity to evaluate systemic risk.

Beyond the regulatory data gaps identified by the FSB, there are also questions about wider market transparency. Limited visibility can mean that creditors have little sight of deteriorating standards or borrowers' arrangements across their range of creditors.

3. Good governance and reporting

The growing interest in private credit is expected to place increasing pressure on supervisors to review and strengthen reporting requirements, which may give rise to new regulatory guidelines. In the UK, the FCA is anticipated to undertake a review of AIFMD reporting obligations, whilst the EU will expand its existing reporting framework under AIFMD II with the aim of reinforcing consistent, high standards across private markets.

One of the key areas the BoE is exploring is the quality of governance practices, with the SWES exercise designed to test what decisions were made, the rationale behind those decisions, and by whom they were taken. Linked to this is the FCA's heightened focus on valuation practices and conflicts of interest, with targeted reviews of firms having been carried out over the last 18 months. The FCA has indicated that firms should expect continued "deeper dives" into the industry, and private credit managers should therefore prepare for more frequent touchpoints, more extensive evidence requests, and potentially greater regulatory challenge.

With the potential to see meaningful reform in the UK regulatory landscape this will in turn influence the development of global standards.

Where are the findings likely to take global regulators?

Many global authorities will be keenly awaiting the findings from the BoE’s SWES test. An interim report is expected in 2026, and the final report will be delivered in 2027. The anticipated milestones are as follows:

- the BoE's Financial Stability Report is due on 7 July 2026 and will include early findings from the exercise;

- in Q4 2026, participants will be given the opportunity to provide feedback on initial findings and evaluate their responses. The BoE will take the assumptions made by private capital fund managers and share those with the banks and institutional investors involved in the programme. It will then share the banks' responses back with the fund managers, enabling them to re-evaluate their initial positions; and

- the final report is expected to be published in 2027. This is the report that global regulators and supervisors are anticipated to use as a springboard for policy reform.

The conclusions are expected to be qualitative rather than policy-prescriptive, though the findings will be shared with other policymakers.

The US Federal Reserve's May 2026 Financial Stability Report identifies private credit as one of the most widely cited near-term risks to financial stability, however the US Federal Reserve's own assessment is relatively measured. The report notes that, whilst evergreen private credit vehicles faced notable increases in redemption requests in late 2025 and early 2026, most managers chose to cap redemptions at 5% of net asset value. The report concludes that "risks to financial stability from further redemption requests appear limited and manageable". A major catalyst for regulatory attention is the democratisation of access to private credit. The US Securities and Exchange Commission's (SEC) Chairman, Paul Atkins, has indicated support for "reasonable retailisation" of private credit markets, signalling that the SEC views expanding retail access as broadly positive but warrants appropriate guardrails. On balance, the US appears to favour expanding access to private markets, however, the sector is likely to face heightened monitoring.

The European Central Bank's most recent and comprehensive assessment of private credit was also published in May 2026 as a special feature within its Financial Stability Review. Its findings are consistent, concluding that direct bank lending to private credit funds is relatively small but that data challenges, multiple layers of leverage and growing interconnections with insurers warrant close ongoing monitoring.

The following areas are likely to attract sustained regulatory attention.

Governance standards

Supervisors are expected to focus on the adequacy of decision making by management and the frameworks in place to support investor outcomes. This could test the substance behind governance structures, examining board and committee minutes, escalation records, and evidence of challenge at a senior level. In practice, this means assessing whether investment committees are genuinely scrutinising individual credit decisions or merely ratifying recommendations, whether there are clear lines of accountability when positions deteriorate, and whether investor outcome frameworks translate into demonstrable action rather than policy documentation alone.

Valuations

The exercise can be considered as part of the wider trend of more regulatory scrutiny of valuation methodology and practices. This scrutiny may move beyond policy review and into sampling of individual asset valuations, testing the inputs and assumptions used at each reporting date.

There is likely to be scrutiny over the degree of separation between portfolio managers and valuation functions. Regulators may review whether third-party valuers are rotated or subject to independence safeguards, and challenge the calibration of discount rates, recovery assumptions, and comparable benchmarks applied to illiquid positions where observable market data is limited or absent or where such data is subject to a higher level of uncertainty in case of distressed market conditions.

Conflicts of interest

Supervisors may explore economic flows and associated decision-making across affiliated entities, testing whether conflicts registers capture real-world arrangements rather than generic risk categories. In practice, this is likely to involve examining specific instances of related-party lending or co-investment allocation, reviewing whether fee-sharing arrangements between management company affiliates are disclosed and appropriately governed, and assessing whether a firm’s monitoring programme can detect conflicts as they arise rather than relying solely on periodic tests.

Underwriting and liquidity management

Supervisors are likely to examine the end-to-end credit process, from initial origination through to watchlist management and workout. In practical terms, this could mean reviewing underwriting files for consistency of credit criteria, testing whether borrower covenants are actively monitored or only reviewed at refinancing, interrogating the severity and frequency of stress test scenarios applied to portfolios, and evaluating how concentration limits and refinancing timelines are tracked against fund-level liquidity positions.

Communications to investors

Regulators may review disclosures to investors, not merely for technical compliance but for whether they enable investors to make properly informed decisions. In practice, supervisors are likely to test whether marketing materials and investor reports present a balanced picture of downside risk alongside performance, whether fee waterfalls and carry mechanics are explained with sufficient clarity, and whether redemption terms and gating provisions are disclosed in a manner that reflects the realistic liquidity an investor can expect, particularly where funds are distributed to non-institutional participants.

1 The list of participants can be viewed on the Bank of England’s website.

Authors

Related topics

Like what you are reading?

Stay up to date with our latest insights, events and updates – direct to your inbox.

How can we help you?

Browse our people by name, team or area of focus to find the expert that you need.