/Passle/MediaLibrary/Images/2026-01-09-17-39-28-122-69613d501e42b4e613742ef5.jpg)

The year in UK mergers: trends and highlights from 2025/26

13 minute read

The CMA recently released its merger outcomes data for the 12 months up to and including March 2026. In this article, we look at how that data compares to previous years and pick out some key trends and themes from the year’s decisions.

As we noted in last year’s equivalent article, 2024/25 was something of a turning point for UK merger control. The CMA signalled a clear intent to make its enforcement process more proportionate and business-friendly, and this was accompanied by some notable outcomes.

This evolution in policy continued in 2025/26. As we explore below, the CMA appears to be taking an increasingly targeted approach to scrutinising transactions.

2025/26 at a glance

| Phase 1 | Phase 2 |

32 inquiries concluded:

| Four inquiries concluded1:

|

Digging into the data – Phase 1

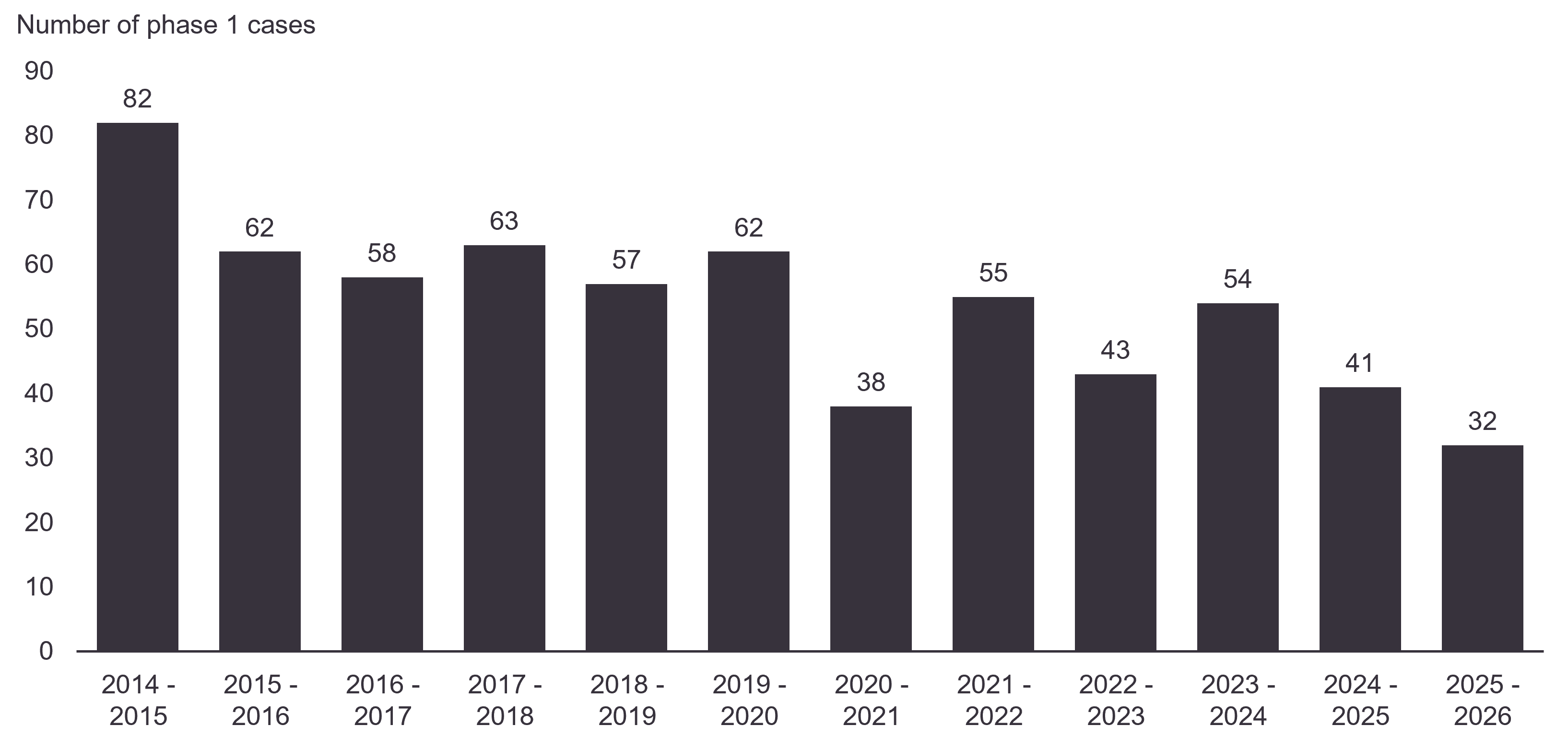

Phase 1 case numbers at all-time low

Source: CMA Merger inquiry outcome statistics; Macfarlanes research.

With only 32 decisions last year (a 22% year-on-year decrease since 2024/25), Phase 1 decision numbers are at an all-time low, continuing the long-term trend since the CMA’s establishment in 2014. The Phase 1 process is increasingly being replaced by the less formal Briefing Paper process, which typically ends with a “no further questions” (NFQ) letter2. The CMA has revealed that 217 Briefing Papers were submitted in 2025/26 – an all-time high, and 30 more than last year. In 2017/18 (the earliest year for which data is available), only 39 Briefing Papers were submitted.

In sum, despite the substantial and continued reduction in Phase 1 decisions, CMA scrutiny of M&A activity remains significant – but is being conducted in a more flexible and targeted way.

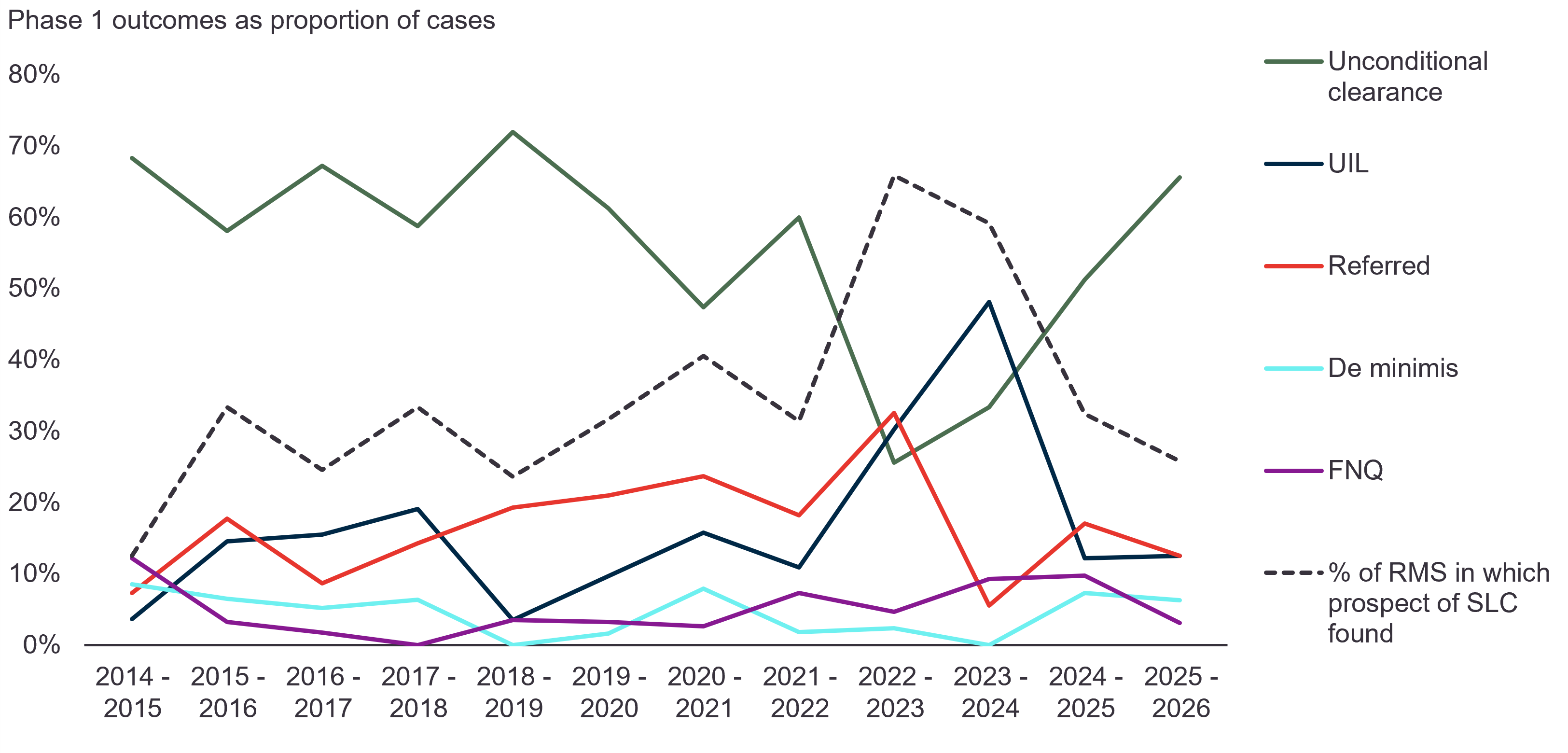

Phase 1 outcomes: a significant increase in unconditional clearances since 2023

Source: CMA Merger inquiry outcome statistics; Macfarlanes research.

Phase 1 outcomes tend to fluctuate year-on-year, depending on the types of transactions coming before the CMA. Over time, however, unconditional Phase 1 clearances became relatively less common, with an overall downward trend in the proportion of cases being cleared without UILs in the period from the CMA’s inception to 2023. The inverse could be observed in relation to cases ending in referral. Both indicated that Phase 1 outcomes were, overall, becoming less favourable to merging parties.

The years since 2023 have reversed that trend. Unconditional clearances are almost back to their all-time high of c. 70% (in 2018/19). Referrals have fallen slightly and are well below their peak in 2022/23 (when 14 of 43 cases were referred). The proportion of relevant merger situations (RMS) in which a substantial lessening of competition (SLC) was found (therefore resulting in a referral decision or the agreement of UILs) has also continued to fall, back down to levels not seen since 2018/19.

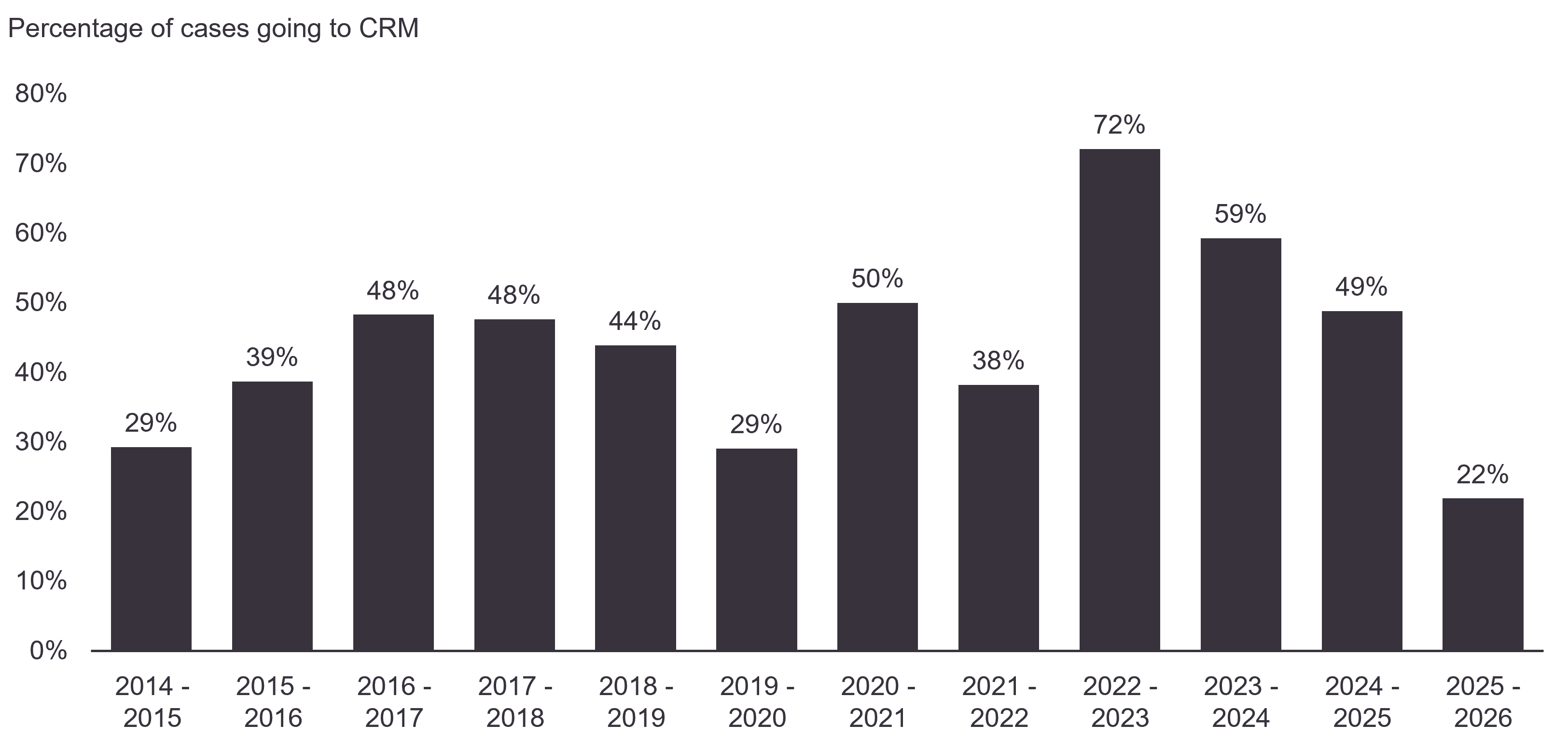

The CMA is being very selective about which cases to scrutinise closely

Source: CMA Merger inquiry outcome statistics; Macfarlanes research.

A case review meeting (CRM) is an internal CMA meeting held after an issues meeting with the merger parties. At an issues meeting, the CMA sets out any concerns it might have about the transaction, to enable the parties to respond to them before a finding of an SLC is reached.

The proportion of cases going to a CRM has fallen dramatically since its 2022/23 peak, closely tracking the decline in cases resulting in an SLC finding. This reveals that, as well as outcomes improving for merger parties, they are also benefitting from a lighter touch process, as preparing for an issues meeting and drafting a response to the CMA’s issues letter are typically very burdensome for parties and their advisors.

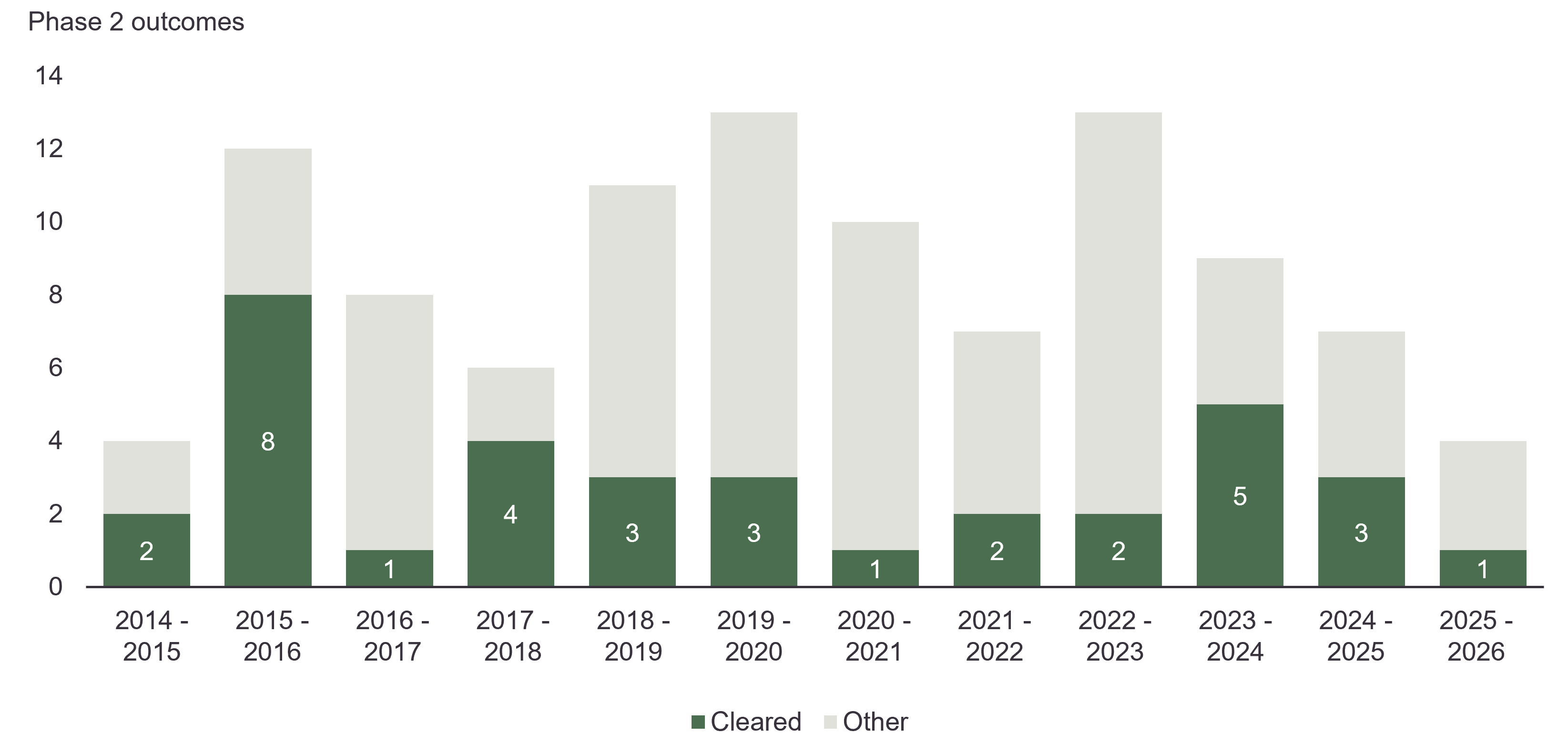

Digging into the data - Phase 2

A low number of Phase 2 decisions – with a low proportion of unconditional clearances

Source: CMA Merger inquiry outcome statistics; Macfarlanes research.

Phase 2 sample sizes are always small, but last year’s was particularly so. Phase 2 decision numbers dropped to four – a level not seen since the CMA’s first year in operation. One of those was the remittal decision in Spreadex/Sporting Index, so only three mergers were looked at de novo. Still, the rate of intervention was relatively high, with only one unconditional clearance.

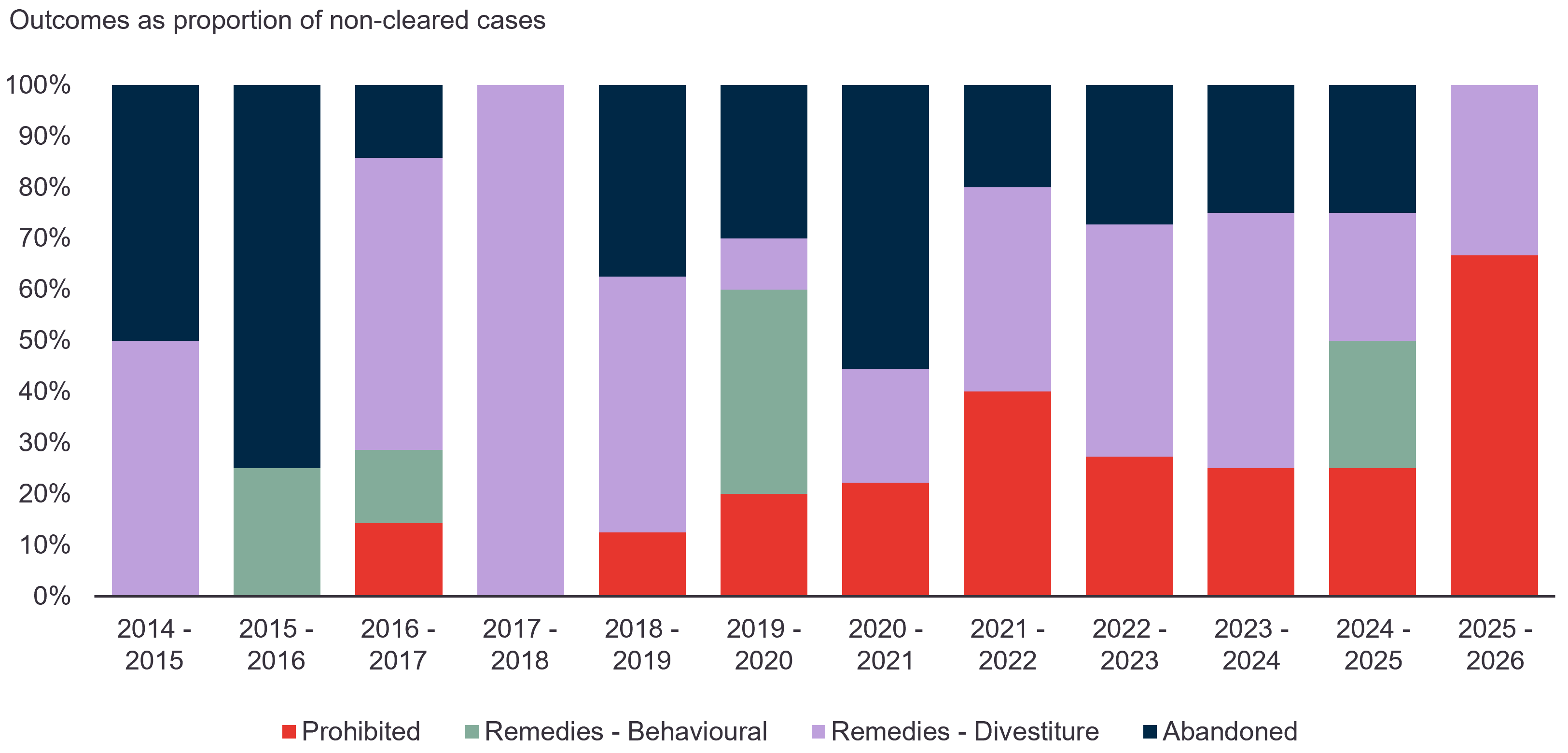

An uptick in prohibitions (on paper at least)

Source: CMA Merger inquiry outcome statistics; Macfarlanes research.

Based on the data alone, last year was a significant outlier in terms of the proportion of Phase 2 interventions that resulted in a prohibition. Whereas prohibition decisions remained relatively uncommon and broadly stable over the preceding eight years, in 2025/26 they accounted for two-thirds of non-cleared transactions. However, as noted above, one of those prohibition decisions was the Spreadex/Sporting Index case3, which was remitted to the CMA by the Competition Appeal Tribunal (having been initially prohibited by the CMA in 2024/25). Leaving this case aside, there was only one prohibition decision last year (Aramark/Entier), which is consistent with each of the preceding two years.

Phase 1 thematic review

As with 2024/25, CMA scrutiny largely focused on traditional, horizontal theories of harm. Whilst around a quarter of Phase 1 cases involved vertical elements, in only one case (Schlumberger/ChampionX - discussed below) did they lead to a finding of an SLC, or even a CRM being held.

The CMA’s Mergers Intelligence function (MIF) appears to have been less active in calling in transactions for review in 2025/26. Based on the published decisions, only nine of the CMA’s 32 Phase 1 cases were called in by the MIF (down from 26 out of 41 cases the year before) – whether following the submission of a Briefing Paper, or on an ex officio basis (the decisions do not specify this4). Given the record number of Briefing Papers the CMA received, it seems the MIF is being very selective about which cases it chooses to call in for a more thorough examination.

New jurisdictional tests being felt

The Digital Markets, Competition and Consumers Act 2024 made material changes to the UK merger control regime’s jurisdictional tests. These entered into force on 1 January 2025, but took some time to manifest themselves in CMA decision-making.

In November 2025, S&P Global/ORBCOMM AIS became the first transaction to be caught by the UK’s new “hybrid” test, which applies where one party (in practice the acquirer) has a share of supply above 33% and a UK turnover exceeding £350m, and the other party has a UK nexus. The CMA examined vertical theories of harm in this case, but cleared the transaction unconditionally.

On the other hand, Kpler/Spire Global was the first transaction formally to be recognised as benefitting from the new “safe harbour” threshold, according to which a merger is not subject to UK merger control if no parties have a UK turnover over £10m. The MIF had called in the transaction on the understanding the threshold was exceeded, but the parties later submitted new information showing that their UK turnover in fact fell below £10m, and the CMA agreed the transaction did not qualify for investigation.

The impact of the 4Ps can clearly be seen

The CMA’s 4Ps (pace, proportionality, predictability, and process) initiative was first revealed toward the end of 2024. Although it was not formally enshrined in the CMA’s mergers procedural guidance until October 2025, its influence began to be felt well before then, as noted in our equivalent article last year, with swifter, shorter Phase 1 decisions.

That trend has since accelerated. Straightforward cases now result in the publication of very short (six or seven page) decisions, akin to the summary decisions the CMA used to publish. Although perhaps not optimal from a transparency perspective, this saves the CMA considerable time. Many cases are being cleared three, or even four, weeks ahead of the statutory deadline.

The average length of pre-notification has also come down significantly, from 71 to 57 working days5. And in 100% of cases where the parties did not opt out of the CMA’s new 40 working-day pre-notification target, that target was met.

CMA (again) able to see past some very high shares of supply

For example, in FIS/TSYS, the merging parties’ combined share of the supply of outsourced credit card issuer processing in the UK was 70-80%. However, no SLC was found as the increment was very small (below 5%) and evidence showed the parties did not compete closely: their customer bases differed significantly, and bidding data showed the parties were seldom rivals for contracts.

Greencore/Bakkavor ended in UILs being accepted, but the parties were able to avoid an SLC finding in respect of the supply of chilled ready meals, despite a 70-80% combined share and a >30% increment. This was because Bakkavor’s large share stemmed from a single customer, and other potential customers did not view it as having a strong offering.

In Beacon Rail/Eversholt, the CMA concluded that there was currently limited competition between the parties, despite them accounting for 50-60% of leasing of freight locomotives in Great Britain. This was primarily because the parties’ assets were tied up in long-term leases and, given the timing of lease renewals, they had not competed head-to-head in the past decade.

Phase 2 thematic review

As noted above, 2025/26 was an especially quiet year for Phase 2 mergers. All four cases looked exclusively at horizontal theories of harm.

CMA still prepared to intervene where competition concerns cannot be ruled out

The shift in CMA merger policy since it came under increasing government pressure to adopt a more investor-friendly stance is undeniable. However, this year’s Phase 2 outcomes demonstrate that the CMA remains willing to intervene where it considers necessary, and that not all mergers will simply be waived through.

Aramark’s completed acquisition of Entier was prohibited after the CMA concluded that it would lead to an SLC in the market for the supply of offshore catering and ancillary facilities management services. The parties were two of the three largest suppliers (together accounting for over 50% of the market) and had lost contracts to only one other supplier. There were also material barriers to expansion and entry, so the parties’ arguments around customer buyer power were rejected. The CMA concluded that the divestment of Entier in its entirety was the only effective remedy (see further below).

In the Spreadex/Sporting Index remittal decision (following Spreadex’s successful appeal of the original decision), the CMA again concluded that a reversal of the transaction was necessary to cure the SLC it identified in the market for the supply of sports spread-betting services. Spreadex’s expanded arguments around the constraints imposed by out-of-market unregulated suppliers, and the impact of the persistently shrinking market for spread-betting, failed to sway the CMA’s final assessment. Spreadex’s arguments on the remedy also fell on deaf ears.

The CMA also imposed remedies in GXO/Wincanton. A counterpoint to the high-market-share Phase 1 clearances mentioned above, the CMA concluded that the parties competed particularly closely in the market for the supply of dedicated warehousing services to grocery customers. In this segment, their share was over 70% and they faced only one other competitor, despite having only a modest share of the broader market. Further, outsourced warehousing presented distinct advantages over self-supply, and opportunities for entry/expansion were limited. The CMA therefore required divestment of Wincanton’s dedicated grocery warehousing business to a suitable purchaser.

Cross-cutting themes

A revised approach to remedies, but the floodgates are not open (yet)

In last year’s article we hailed the return of behavioural remedies, as the CMA cleared Vodafone’s merger with Three, subject to a package of behavioural remedies aimed at locking in rivalry-enhancing efficiencies. This was followed by the launch of a high-profile review by the CMA of its approach to merger remedies more generally, and also a significant outcome in the Phase one case of Schlumberger/ChampionX.

In that case, the CMA accepted a complex package of UILs involving: (i) a business divestment by way of asset transfer with accompanying IP and a transitional services agreement; and (ii) a CMA-approved licensing arrangement to enable a third party to enter and create an alternative source of supply of quartz sensors and transducers, combined with the extension of existing supply contracts in the meantime. Whereas the CMA has traditionally insisted on “clear-cut” remedies at Phase 1 (generally speaking, the sale of a clearly-defined existing business), this case therefore involved both “carve-out” and behavioural remedy elements (you can read more in our previous article).

Toward the end of 2025, the CMA then formalised its new position on remedies by publishing new guidance. This did away with the presumption against behavioural remedies at Phase 1, and recognised a broader range of circumstances in which they can be effective. However, it was not a comprehensive shift in approach – the CMA retains an express preference for structural remedies, and remains very sceptical of behavioural remedies that seek to control outcomes rather than foster competition.

Since Schlumberger/ChampionX, no further behavioural remedies have been agreed. In GXO/Wincanton, the parties proposed to sponsor a new entrant logistics provider, both financially and through the award of two contracts (with divestiture as a backstop should it fail). But the CMA rejected this proposal, concluding that it would not be an effective remedy to the SLC, including because it was too uncertain and lacked relevant third-party support.

Further, in Aramark/Entier the CMA examined several carve-out remedies as an alternative to the full divestment of Entier. These would have involved the transfer of some or all customer contracts of either merging party, together with onshore and/or offshore staff supporting those contracts, to a suitable third party. The CMA concluded that these options would not be effective, due to difficulties in transferring a viable cohort of staff and concerns about the ability of any purchaser to operate on a standalone basis.

Failing firm defences increasingly prevalent

Last year we remarked that there had been a resurgence of the failing firm defence, with exiting firm arguments being accepted in three separate cases at Phases 1 and 2 (compared to only two cases in the preceding six years).

That trend has continued. The CMA cleared two cases on an exiting firm basis at Phase 1: Rundvirke/Calders & Grandidge (concerning suppliers of timber telephone poles) and Sportradar/IMG Arena (concerning sports data feeds). This involves overcoming a significant evidential threshold as, at Phase 1, the CMA needs “compelling evidence” that it is inevitable that, absent the transaction, the failing firm would have exited and there would not have been an alternative, less anti-competitive purchaser for the firm or its assets (whereas, at Phase 2, the CMA needs to conclude that the two limbs of the exiting firm test are met on the balance of probabilities).

However, the CMA rejected an exiting firm argument at Phase 1 in Constellation/ABVR, on the basis that there would have been purchasers for at least some of ABVR’s assets in the market for B2B vehicle auction services. The merger was cleared at Phase 2 on a “partial exiting firm” basis – some of ABVR’s assets would indeed remain in the market, but impose less of a constraint on Constellation than they previously did. The CMA also rejected an exiting firm argument in Getty/Shutterstock, which was conditionally cleared at Phase 2 in mid-May.

Conclusion

In sum, the CMA’s more pragmatic approach to merger assessment has continued from the previous year. It remains willing to intervene where absolutely necessary, so it certainly is not open season for all transactions to be waived through. However, those that appear suitable for Phase 1 clearance are now being approved much more swiftly and efficiently – both in terms of pre-notification and the Phase 1 timetable. More transactions are now also being (informally) “approved" at the Briefing Paper stage.

Perhaps more interestingly, the CMA appears consistently more open to arguments around the relevant counterfactual than it was only a few years ago. On the other hand, it remains to be seen whether behavioural remedies will become commonplace.

As ever, however, one must be cautious when inferring changes in CMA policy or approach from individual decisions. The CMA is always keen to stress that all mergers are considered on their own merits.

Footnotes

1 One decision (Spreadex/Sporting Index) is a remittal decision, following Spreadex’s successful appeal of the original prohibition decision.

2 Following an NFQ letter (which is not made public), the CMA is still able to call in a transaction and require a Phase 1 notification. This tends to occur only once or twice a year, but last year no NFQ letters were followed by a call-in.

3 For these purposes we have included the original decision in the 2024/25 figures, and the remittal decision in the 2025/26 figures.

4 Data separately published by the CMA states that it called in 14 mergers following the submission of a briefing paper in 2025/26. However, this includes cases that had not reached a final resolution or indeed that remained in pre-notification at the year end.

5 This figure is expected to fall further next year as the CMA’s 40 working-day pre-notification KPI only applied to cases where a draft merger notice was received on or after 20 June 2025.

Authors

Related topics

Like what you are reading?

Stay up to date with our latest insights, events and updates – direct to your inbox.

How can we help you?

Browse our people by name, team or area of focus to find the expert that you need.