The expanding role of back leverage: “loan-on-loan” for non-real estate assets

8 minute read

In this article, the authors examine the core structure of “loan-on-loan” transactions and consider how market practice may translate to financing lending and underlying asset classes beyond the real estate realm.

Loan-on-loan

Back leverage, including by way of what are commonly known as “loan-on-loan” financing structures, has fast become a staple of the commercial real estate (CRE) lending market, enabling credit funds and other non-bank lenders to leverage loans originated and made against CRE. While asset-backed lending (ABL), more holistic net asset value (NAV)-based lending and repo structures have been popular with credit funds – and private credit collateralised loan obligations (CLOs) have shown up to offer another potential route to raising finance for non-CRE lending on an aggregated basis – the use of loan-on-loan structures can be considered an alternative.

This article examines the core structure of loan-on-loan transactions and considers how market practice – which up until now has largely been shaped by the CRE lending market – may translate to financing other lending and underlying asset classes.

Core structure

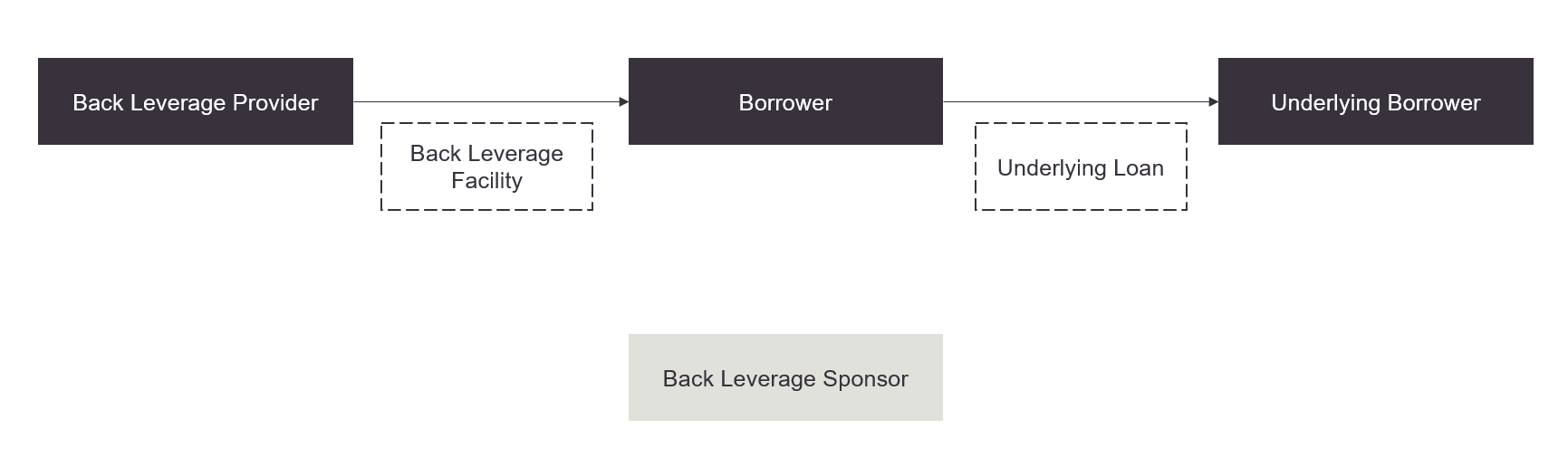

The loan-on-loan structure is centred on an underlying loan. Typically, a credit fund manager (Back Leverage Sponsor) seeking additional financing establishes and (equity) funds a special purpose vehicle (SPV) to act as the lender of record (Borrower) and make a loan (Underlying Loan) to an underlying borrower (Underlying Borrower) for the purpose of acquiring or developing an asset or a portfolio of assets (whether tangible or intangible).

The Borrower uses its rights as lender under the Underlying Loan as collateral to procure a second loan by way of a Back Leverage Facility1 from a Back Leverage Provider. This is typically a more traditional financial institution, usually a bank, which may not want direct exposure to the underlying asset(s) or which is seeking better capital treatment than making the Underlying Loan directly.

Cash payments of interest and principal flow upwards from the Underlying Borrower to the Borrower under the Underlying Loan and are used to make payments to the Back Leverage Provider under the Back Leverage Facility. Financial and other covenants at both levels are focused on the performance and, thus, payments of the Underlying Borrower. The appropriate and sufficient measure of control afforded to the Back Leverage Provider in respect of the Underlying Loan is a significant (arguably determinative, in this type of back leverage) matter and, consequently, often subject to detailed negotiation. We address below some aspects of how this manifests in documentation. (For a more detailed guide to these structures, see our article: “Back leverage – a deep dive”.)

Figure 1: A typical loan-on-loan structure

The securitisation question(s)

A key question to be determined by funds looking to import this technology into non-CRE asset classes is whether the transaction qualifies as a securitisation for the purposes of EU and UK regulation, which could enable the Back Leverage Provider to benefit from more favourable capital treatment afforded to investments in securitisations.

CRE loan-on-loan transactions will often not qualify as securitisations as a result of the “specialised lending” exemption. This is focused on income generated by underlying “physical assets” so, while there is some synthetic expansion of that concept to consider (where physical assets may not, technically, underlie but there is an “economically comparable exposure”), the exemption will not apply to all asset classes for which back leverage may be provided.

Where the exemption does apply, or the transaction does not qualify as a securitisation for another reason, this would alleviate a compliance burden (as to mandated due diligence, disclosure and risk retention requirements, in particular2). However, the intricacies of comparative capital requirements could still determine whether this outcome is, on balance, desirable from the Back Leverage Provider’s perspective – lower capital requirements might be considered essential for exposures that generally must be held to maturity, in the absence of a market or mechanism for syndication or securitisation of the Back Leverage Facility.

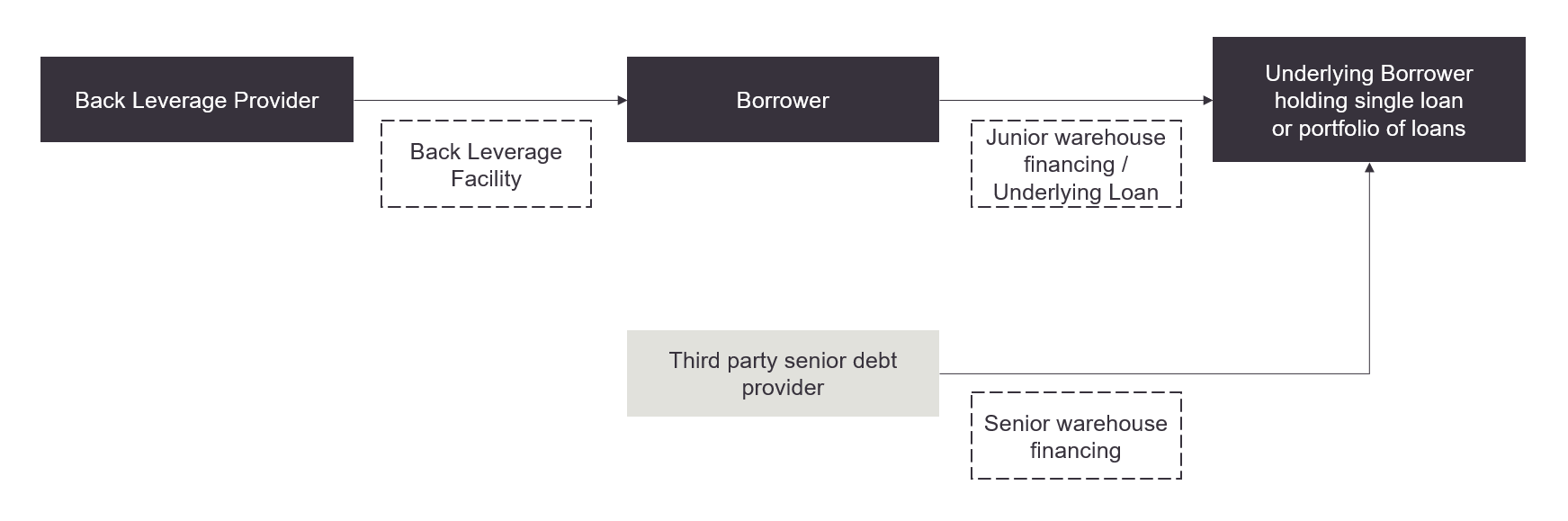

In short: the regulatory position, and its consequences, are not always clear, especially when considering the financing of different asset classes. And they will require even more attention if the Underlying Loan is already part of a securitisation. For example, the Underlying Loan may be a junior tranche of a warehouse financing arrangement – as suggested in Figure 2 below – that already qualifies as a securitisation. Resecuritisation (in this case, involving tranched funding coming in at the back leverage level) is generally prohibited, and so the loan-on-loan arrangement (the back leverage) cannot also qualify as a securitisation if it is to be regulatorily compliant.

Figure 2: Example loan-on-loan structure with an underlying warehouse financing arrangement

There are ways in which a (re)securitisation might be avoided:

- The credit fund(s) managed by the Back Leverage Sponsor not providing funding to the Borrower in the form of debt. “Equity” funding in the shape of subscription for interests in the fund, and onward subscription for shares in the (SPV) Borrower, may be acceptable to some Back Leverage Providers running the rule over the regulatory implications of a proposed transaction. One of the criteria for a securitisation is that the credit risk is tranched. Structural subordination (as equity is to debt), rather than contractual subordination, assists in rebutting this criterion being satisfied.

The Back Leverage Provider’s recourse being wider than just to payments derived from the Underlying Loan (and, ultimately, the loan(s) held by the Underlying Borrower). The Back Leverage Provider might benefit from security over: i) shares in the Borrower, granted by the shareholding fund managed by the Back Leverage Sponsor; ii) receivables owing from the Borrower to that shareholder, the Back Leverage Sponsor and any associate; and iii) all assets of the Borrower.

In some cases, the Back Leverage Provider might benefit from fuller recourse to the fund(s) managed by the Back Leverage Sponsor in the form of a (limited or unlimited) guarantee.

Another criterion for a securitisation is that payments in the transaction are dependent on the performance of the underlying exposure or pool of exposures. In situations where additional recourse is available from the Borrower or the Back Leverage Sponsor, including by way of guarantee, this can break the chain between performance of the underlying assets and payments made under the Back Leverage Facility3.

Due diligence and key documentary provisions

Similar to lending under a CRE loan-on-loan, Back Leverage Providers will expect:

- comprehensive due diligence on the underlying asset or portfolio of assets, and a satisfactory understanding of the credit position of the Back Leverage Sponsor and its relevant fund(s);

- the ability to review and comment on the terms of the Underlying Loan, an understanding of the security package and reliance on all reports and legal opinions provided in connection with the Underlying Loan;

- in the Back Leverage Facility: i) a pass-through of the on-going information rights, and reports and other information received under them, which are provided to the Borrower as the lender of the Underlying Loan; ii) if the Underlying Loan involves a forward flow or continuous origination aspect, a review or veto of, or at least input to, the eligibility criteria controlling which new loans or receivables are originated or purchased and sold into the structure; and iii) representations from the Back Leverage Sponsor in respect of the underlying portfolio, mirroring key representations given by the Underlying Borrower; and

- in respect of the Underlying Loan: i) a reserved matters regime, and control of any provisions which could permit amendments to the economic terms of the connected transaction – requiring Back Leverage Provider consent; and ii) control of any waivers of events of default that could be granted by the Borrower to the Underlying Borrower.

The documentary regime can be intricate. This reflects the nature of the loan-on-loan structure: although it is a financing (rather than risk management) tool for a Back Leverage Sponsor to obtain leverage at scale, it is closer than more aggregated4 financing arrangements to a (funded) sub-participation in its specific focus on the detailed terms of the Underlying Loan and the dynamic between the Borrower and the Underlying Borrower. Whether there should be an adjustment of the Back Leverage Provider’s control over the Underlying Loan and, ultimately, the underlying asset(s) which is commensurate with the measure of wider recourse it has to the Back Leverage Sponsor is an interesting commercial matter. Its resolution is likely to be deal-specific, which is one reason why establishing a programme for the provision of back leverage for Underlying Loans can be time well spent if it avoids protracted negotiation of terms each time back leverage is sought from the same Back Leverage Provider.

Looking ahead

However defined, the market for back leverage is steadily increasing in size, with new providers entering the market in traditional and novel ways. While the CRE back leverage market has been a proving ground for the core structural and documentary features of these transactions, the extension of loan-on-loan financing to non-CRE assets represents a natural evolution.

While the fundamentals remain the same, practitioners will need to pay close attention to the securitisation analysis, the specific eligibility criteria for the underlying portfolio and the nature of the underlying asset class.

Footnotes

1 Which facility may be programmatic in nature – providing a framework for back leverage to be made separately available for a number of Underlying Loans.

2 That said, if the Back Leverage Sponsor is an alternative investment fund manager (AIFM) and the relevant fund is a “loan-originating AIF” subject to regulation as such in the EU, similarly granular rules as to risk retention and operations could bear on the Underlying Loan and a cap on fund leverage could bear on the feasibility and economic terms of the Back Leverage Facility (dependent on whether and how there is recourse to the fund).

3 However, such recourse should, where relevant, be considered in view of the cap on fund leverage mentioned in footnote 2.

4 Often NAV-based.

This article was first published in the June 2026 issue of Butterworths Journal of International Banking and Financial Law.

Authors

Related topics

Like what you are reading?

Stay up to date with our latest insights, events and updates – direct to your inbox.

How can we help you?

Browse our people by name, team or area of focus to find the expert that you need.