Partnership profit allocations in Walewski v HMRC

01 April 2020This article considers the implications of the decision for fund managers.

In January 2020, the First-tier Tax Tribunal considered, for the first time, the “mixed partnership” rules that were introduced in 2014 to combat excess partnership profit allocations to a company rather than an individual (generally if made in order to reduce the individual’s personal tax bill).

Fund management (and other) firms with a UK limited liability partnership (LLP) in their management structure should review the participation of companies in the LLP and consider: (i) how the companies justify their profit allocations from the LLP; and (ii) how employment arrangements with executives and advisory arrangements between management entities and funds are documented. If these arrangements go wrong, individual LLP partners could, under the mixed partnership rules, be taxed on profits currently allocated to companies.

Mixed partnership profit allocations in Walewski v HMRC

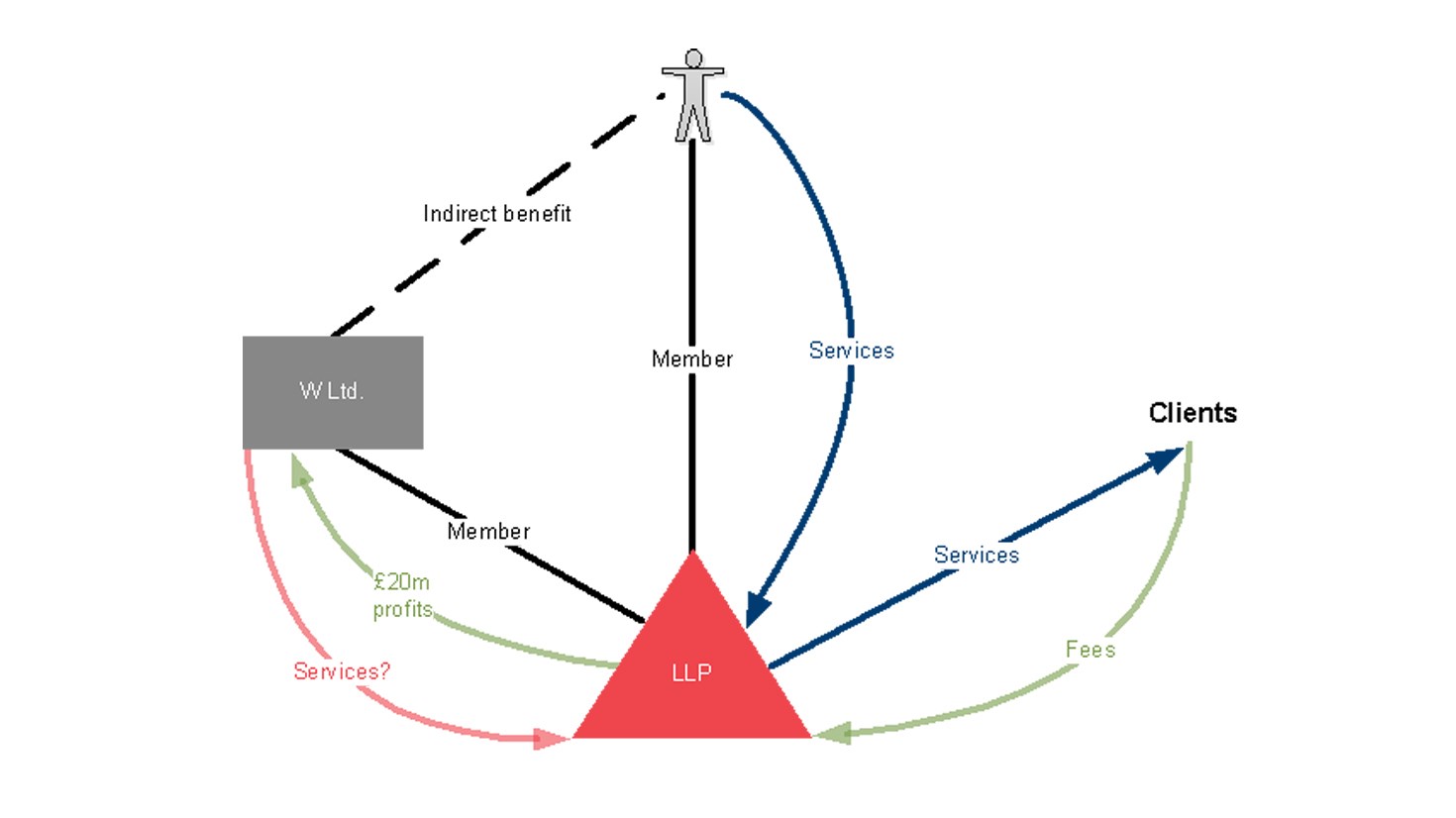

In the case of Walewski v HMRC [2020] UKFTT 58 (TC), the taxpayer (W) had established a Luxembourg private equity fund managed by two UK LLPs in which W was a partner. W had also set up a company (W Ltd.) which was a corporate member of each LLP. W was the sole director and employee of W Ltd. W provided services to clients as: (i) partner in the LLPs; and (ii) director/employee of W Ltd.

HMRC assessed W to income tax on £20m of profits that had been allocated to W Ltd. by the LLPs. These profits were reallocated to W under the mixed partnership rules (contained in s.850C ITTOIA 2005) on the basis that the profits had really been allocated to W Ltd. as a result of W’s power to enjoy them through W Ltd.’s ownership structure (an offshore trust from which W could benefit), rather than being earned by W Ltd. in exchange for services provided to the LLPs.

W appealed the assessment, arguing that the profits were earned by W Ltd. in respect of work done by W as an employee of W Ltd. The Tribunal dismissed W’s appeal, finding that the profits allocated to W Ltd. by the LLPs could not be explained by W’s activities as an employee of W Ltd.

There was not enough evidence that W had provided services to clients as an employee of W Ltd. rather than a member of the LLPs. Instead, the Tribunal found that:

- W had been working full-time for the company and the LLPs simultaneously;

- his work as an employee of W Ltd. could not be separated in a way that justified the allocation of LLP profits to the company; and

- the real explanation for the allocation of profits to W Ltd. was W’s ability to enjoy the profits.

As a result the profits were properly reallocated to W.

Implications for fund management (and other) firms

This is the first time the Tribunal has considered the mixed partnership rules and may encourage HMRC to challenge other mixed partnership arrangements.

The mixed partnership rules were introduced in 2014 to combat excess profit allocations to companies that are partners in partnerships alongside individuals (i.e. mixed partnerships). The rules apply where a company in which an individual partner has an interest is allocated excess profits due to the ability of the individual to enjoy those profits.

Review current arrangements: Fund managers with LLPs in their structures should (re‑)consider these rules, particularly where management or holding companies owned by a relatively small group of individuals participate in the LLPs alongside some of the same individuals and/or individuals take below-market remuneration from the LLP or from their employment.

Documentation: Firms should ensure that employment agreements between such companies and individual employees are in place where needed, and that the basis on which such companies justify their profit allocations is clear and properly recorded. For instance, advisory agreements should make it clear when the company is providing services to the LLP or when the company rather than the LLP is providing services to a client. Informal arrangements are more likely to trip over these rules, potentially resulting in taxable profits being attributed to individual partners.

Context is important: It was also relevant to the Tribunal’s findings that W drew a salary from W Ltd. that was “modest in terms of the industry in which he worked” and did not take a bonus, suggesting to the Tribunal that W must have expected to enjoy W Ltd. profits. This might suggest that the presence of a market-rate salary would have taken some pressure off a reallocation of profits under these rules by making it easier to demonstrate a different commercial reason for the allocation of profits to the company.