/Passle/5a1c2144b00e80131c20b495/MediaLibrary/Images/2025-09-04-13-40-36-827-68b996d45a0e7c387a35d0f9.png)

Employment tax update - May 2023

3 minute read

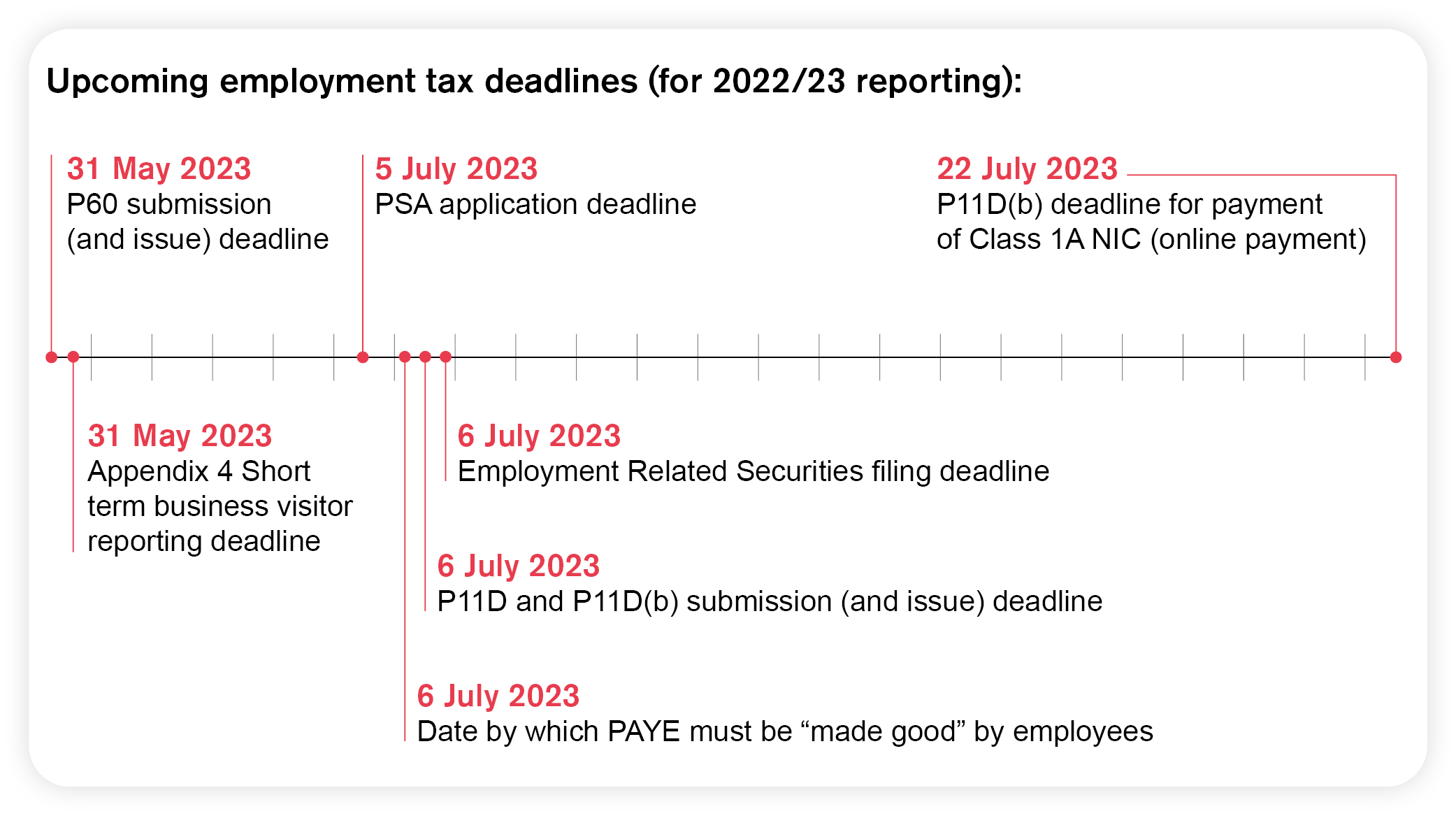

On the back of the regular HMRC agent updates we will be releasing a monthly bulletin setting out changes to legislation and HMRC guidance, as well as upcoming deadlines and key areas of focus relevant to employment taxes and reward activities.

Our first bulletin follows the release of the April HMRC Agent Update (Issue 107) and summarises updates on off-payroll working, fixing problems with running payroll, Time to Pay arrangements, homeworking deductions and termination payments.

Update to HMRC guidance for off-payroll working (IR35) to offer increased clarity for those engaging contractors.

- Overall, the rules on off-payroll working have not changed, however HMRC have updated their guidance to make it easier to understand and to use for those who need it.

- HMRC also offer some pointers on record keeping and provide a link to their off-payroll guidance for clients.

- For further off-payroll working related updates, you can also read our commentary on the Gary Lineker and Eamonn Holmes IR35 cases.

Update to the "fix problems with running payroll" guidance and new process coming soon for overpayments of National Insurance contributions.

- Employers should still correct overpaid National Insurance contributions and submit a revised Full Payment Submission.

- Further guidance will be issued in May on how to fix problems with running payroll including details of how to submit applications via PAYE online.

- In addition, a new process for employees or former employees who have overpaid and whose employer cannot correct this for them will also be published.

Update to the assessment year for Time to Pay arrangements for disguised remuneration and the loan charge.

- HMRC have updated the assessment approach used when determining customers' eligibility for automatic Time to Pay arrangements in relation to disguised remuneration settlements and the loan charge.

- HMRC will now use available information from the most recent complete tax year to determine eligibility, determine a "more current picture" of the financial position of customers and to better understand customers' ability to pay.

- Read the full details on HMRC's standard Time to Pay offer.

Update to HRMC guidance to clarify the eligibility criteria for homeworking deductions for expenses and benefits.

- The rules on receiving tax relief for those working from home have not changed, however HMRC have updated their guidance to make the eligibility criteria clearer in the wake of pandemic restrictions being lifted (and the expected number of people eligible for relief falling).

Given the changes to the rules in the past 5 years HMRC want to increase awareness of the tax and National Insurance treatment of termination payments, specifically in relation to the following:

- the introduction of post-employment notice pay;

- the removal of foreign service relief on termination payments to UK resident individuals;

- clarification that the exemption for injury does not apply to injury to feelings; and

- alignment of the rules for income tax and National Insurance contributions.

For further information on the taxation of termination payments you can read the HMRC guidance.

Authors

Related topics

Like what you are reading?

Stay up to date with our latest insights, events and updates – direct to your inbox.

How can we help you?

Browse our people by name, team or area of focus to find the expert that you need.